DOWNLOAD

DOWNLOAD

The Asian Development Bank (ADB) slashed its growth forecasts for the Philippines for this year and 2026 but it is still expected to be the second-fastest growing economy in Southeast Asia.

In its December Asian Development Outlook (ADO), the multilateral lender slashed its Philippine gross domestic product (GDP) growth forecast to 5% from 5.6% in September.

For 2026, the ADB trimmed its Philippine growth forecast to 5.3% from 5.7% previously.

These latest projections are below the government’s 5.5-6.5% target for this year, and the 6-7% growth goal for 2026 to 2028.

In its report released on Wednesday, the ADB said the lower growth prospects for the Philippines were “due to weak infrastructure spending amid investigations of publicly funded projects, and natural hazards.”

Data from the Department of Budget and Management showed that expenditure on infrastructure and other capital outlays for the January-to-September period declined by 10.7% to P877.1 billion from P982.4 billion a year ago.

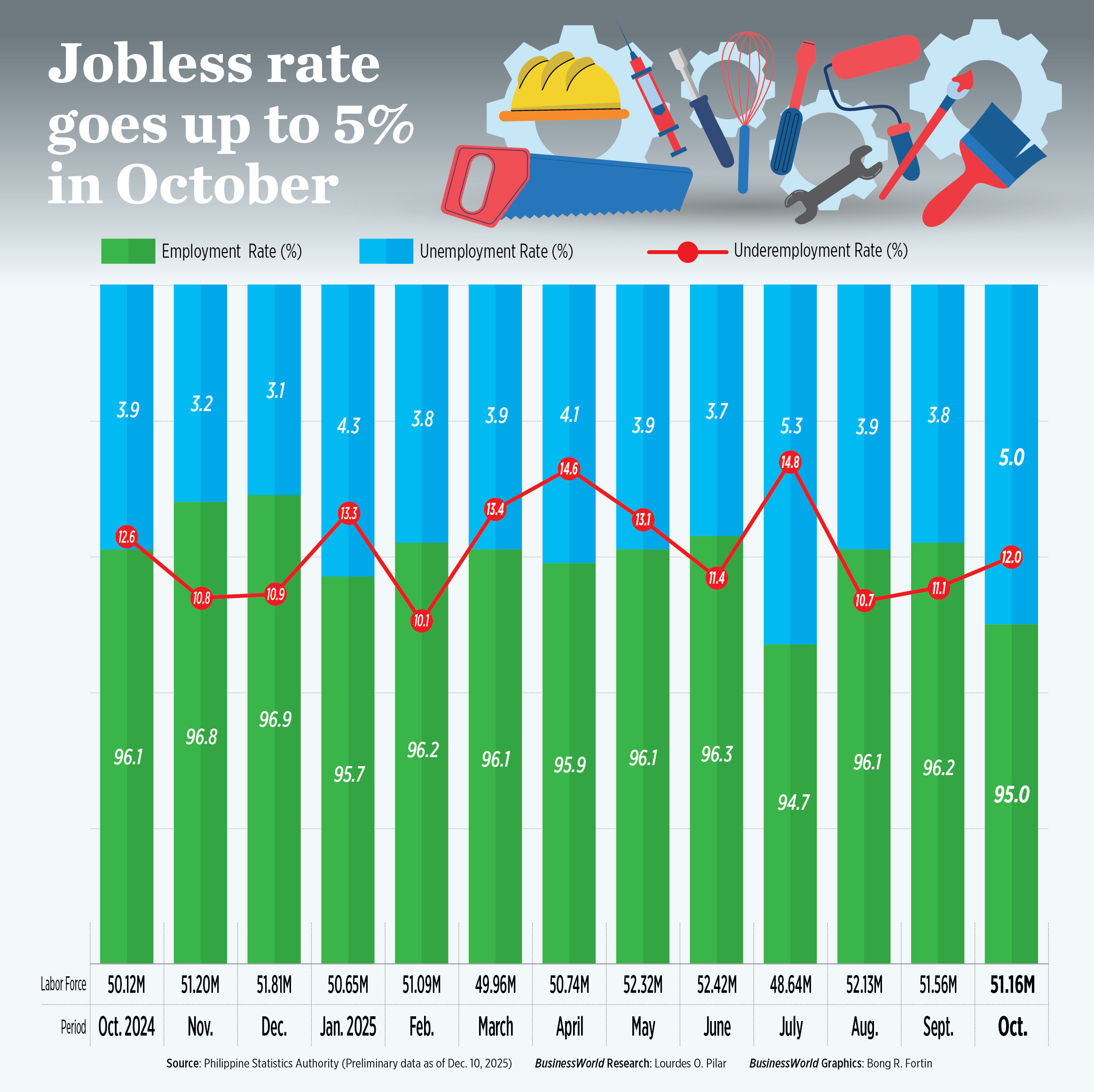

Sluggish infrastructure spending, affected by adverse weather and stricter fund releases to the Department of Public Works and Highways, dragged Philippine GDP growth to a weaker‑than‑expected 4% in the third quarter. This brought the nine‑month average growth to 5%.

“Low inflation and ongoing monetary easing should sustain domestic demand, supporting stronger growth in 2026,” the ADB said.

The Bangko Sentral ng Pilipinas has so far reduced borrowing costs by a cumulative 175 basis points (bps) since it began its easing cycle in August last year, bringing the key rate to 4.75%.

“However, uncertainties arising out of investigations of publicly funded infrastructure projects and weather-related disruptions pose downside risks,” it added.

A corruption scandal involving anomalous flood control projects has already triggered protests, slowed economic activity, and shaken investor confidence in the country.

An independent commission is now investigating the allegations that government officials, lawmakers and contractors received billions of pesos in kickbacks from anomalous projects.

STILL SECOND FASTEST

Based on the latest ADO, the Philippines is still projected to be the second fastest-growing economy in Southeast Asia this year, just behind Vietnam (7.4%) and tied with Indonesia (5%). It is ahead of Malaysia (4.5%), Singapore (4.1), and Thailand (2%).

For 2026, the Philippines is still seen to post the second-fastest growth in Southeast Asia, after Vietnam’s 6.4%.

The ADB expects Philippine growth to stay above the Southeast Asian average through 2026.

For the region, the bank raised its regional GDP growth outlook to 4.5% this year from 4.3% in its September update. It also hiked its projections to 4.5% in 2026 from 4.4% previously.

This reflects stronger‑than‑expected third‑quarter results in Indonesia, Malaysia, Singapore, and Vietnam, alongside better external environment and supportive government expenditures, the ADB said.

“Several risks to the subregion’s (Southeast Asia) prospects remain, notably from global uncertainty, climate-related disruptions, and domestic political developments,” the ADB said.

Despite these risks, the lender said the Southeast Asian region remains resilient, with prospects depending on sustained policy support and flexible economic strategies.

However, the ADB’s Philippine growth forecast was slightly below the projected 5.1% growth of developing Asia for this year but exceeded the 4.6% growth forecast in 2026.

Developing Asia includes 46 Asia-Pacific countries, but excludes Japan, Australia, and New Zealand.

Meanwhile, the ADB expects Philippine headline inflation to average 1.8% this year and 3% in 2026, unchanged from its September forecast.

This is slightly higher than the Bangko Sentral ng Pilipinas’ (BSP) 1.7% average forecast for this year, but lower than the 3.3% average forecast for 2026.

Headline inflation averaged 1.6% in the first 11 months of 2025, according to the Philippine Statistics Authority.

Meanwhile, the Mastercard Economics Institute (MEI) gave a 5.6% growth forecast for the Philippines in 2026, which will make it the fastest-growing economy among the Association of Southeast Asian Nations-5 (ASEAN-5).

This is ahead of Indonesia (5%), Malaysia (4.2%), Singapore (2.2%), and Thailand (1.8%).

“In 2026, the growth trajectories of the ASEAN-5 nations are expected to diverge. GDP is projected to expand steadily in Indonesia and the Philippines, while Malaysia, Singapore, and Thailand may grow more slowly,” MEI said in its December Economic Outlook 2026.

MEI also expects Philippine inflation to settle at 2.8% next year.

“Because that is within the target range, further monetary policy easing may be possible; interest rates are expected to fall to 4.5% by the end of 2026,” it said.

MEI said strong borrowing momentum may fuel private consumption, while lower policy rates may help sustain this trend.

The report noted travel is a key economic driver, with domestic demand climbing in Malaysia and Indonesia and outbound spending rising in Singapore, Malaysia, Indonesia, and the Philippines.

MEI said Indonesia and the Philippines posted the fastest growth gains, with overseas travel spending jumping by 40% and 28%, respectively, over the period, MEI said. — Aubrey Rose A. Inosante