DOWNLOAD

DOWNLOAD

Tag: US 10-year yields

Technical Analysis: The bright side or cautionary tale of disinflation

Learn about the possible benefits and cautions of disinflation to guide your investment strategy. Read this article for more information.

By Kyle Tan

By Kyle Tan

The US Federal Reserve has now reached a pivotal point for the US economy as the restrictive policy rates start to pinch consumer behavior and sentiment, signaling the cautions of disinflation. For countless times, we have heard that the “US economy is strong and resilient”, but the GDP for the first quarter of the year slowed to 1.4% quarter-on-quarter (QoQ), with personal consumption falling to 1.5%.

Despite US equity markets continuously hitting all-time highs, consumer sentiment has fallen to a 7-month low. The 2-decade-high interest rate environment has divided consumer conditions, with economic gains favoring the wealthy, while the vast majority continues to struggle.

Disinflation is bullish for risk assets

Disinflation is commonly defined as the slowing of inflation. Compared to deflation, disinflation is generally interpreted as a good backdrop for risk assets as “softer economic data would be taken as positive news by markets”. As economic tightening gets fully absorbed by the economy, policymakers are now ready to do the balancing act of bringing the economy back to its neutral growth cycle. Hence, the weakening of resilient data would prompt markets to price in the optimism ahead of the policy easing.

We saw the first half of 2024 pricing risk assets near to perfection. The S&P 500 has beaten targets over and over again as the technology sector single-handedly carried the US index to new highs.

Despite the risk-on regime, early deflationary signals such as falling housing starts and weak manufacturing Purchasing Managers’ Index (PMI) prompted the concentrated equity rally into the mega-cap technology names amid the continuing AI fever.

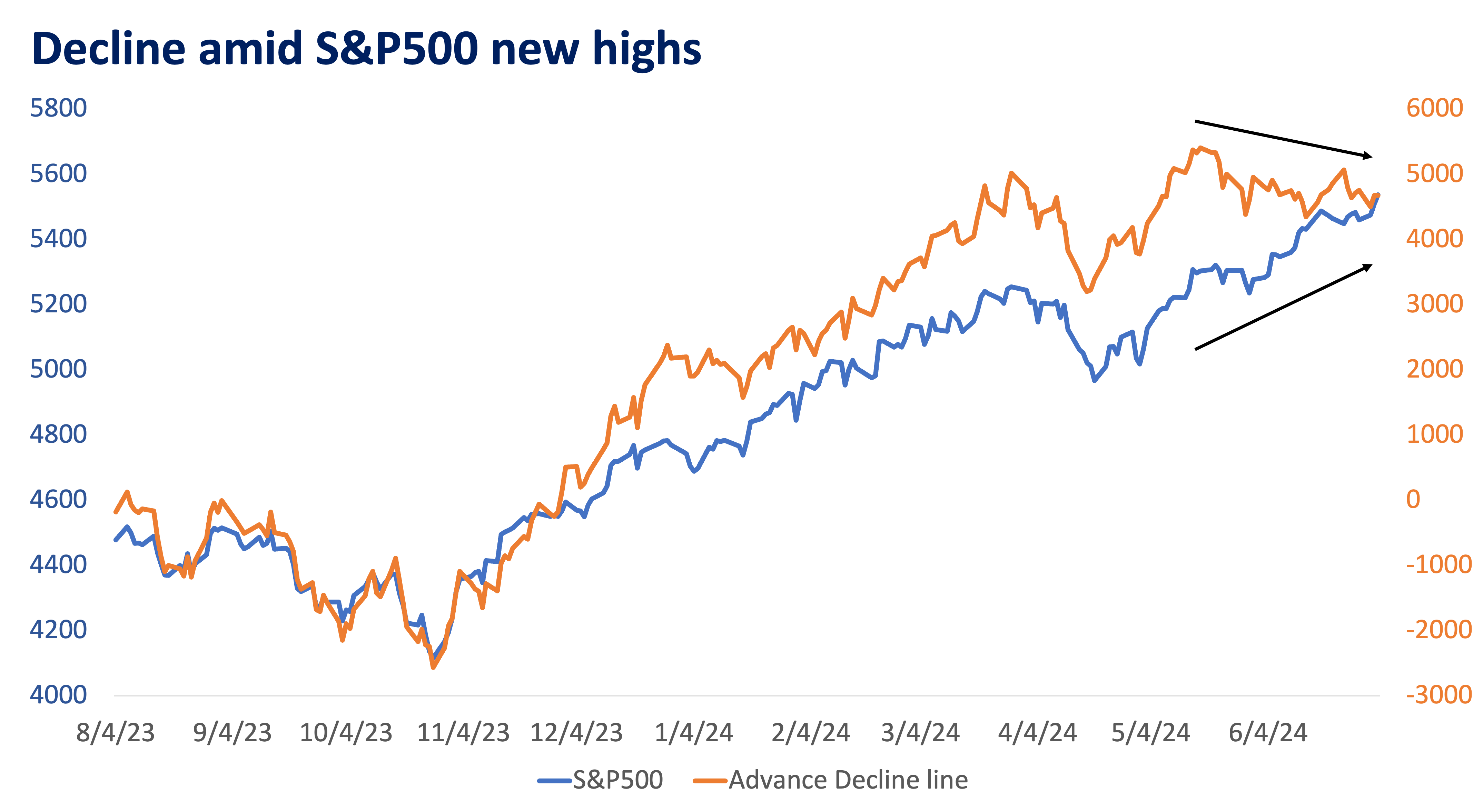

Looking at the chart above, the S&P 500 Index (i.e., blue line) is shown climbing new highs. Meanwhile market breadth (i.e., orange line) as illustrated by the Advance Decline line suggests that stocks participating in the rally are on a downward trend. Along with insider selling, this appears to be a signal of vulnerability near market tops.

So far, the stock market rally has priced in several scenarios:

- The US will have a soft landing; keeping track of inflation shows that it’s gradually falling in line with expectations.

- Technology and company earnings will remain strong, with outlook remaining positive.

- No foreseen adverse black swan events, including the US elections, which shows a more predictable economic scenario.

It is worth highlighting that the absence of any of the above may trigger a reversal of the strong mark-up. A similar event we have observed can be seen in how the S&P 500 easily dropped by 6% in April 2024 when tensions between Israel and Iran risked escalating to superpower allies.

It is worth highlighting that the absence of any of the above may trigger a reversal of the strong mark-up. A similar event we have observed can be seen in how the S&P 500 easily dropped by 6% in April 2024 when tensions between Israel and Iran risked escalating to superpower allies.

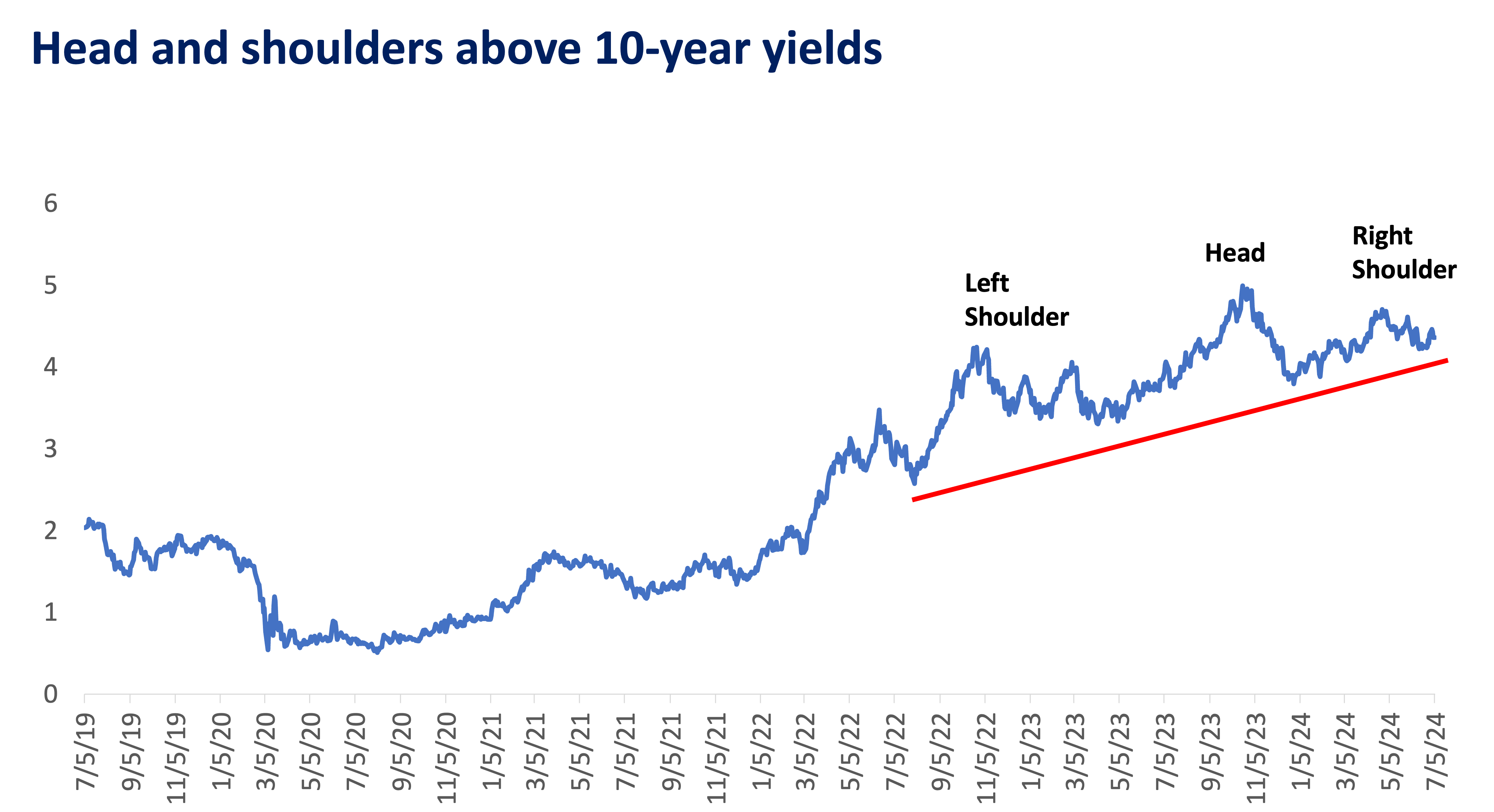

A Head & Shoulders (H&S) pattern has emerged for the historical US 10-year-yield. The signal has a minimum drawdown target of 3.58% to 2.90%, or a decrease in 10-year yields, which currently sit at 4.29%. The completion of the formation and corresponding target levels signal recession risks.

However, this move will not be confirmed and not necessarily acted upon until the yield levels break below the 4.15% support. A confirmed breakdown of a H&S has a 90% probability of hitting its target level.

Takeaway

While disinflation remains a risk-on regime, both the S&P 500 and US 10-year yield have begun to signal a potential shift to risk-off in the coming months or quarters. The 2024 US elections is reflationary in nature, but policy changes post-elections will determine the pace at which we will transition into a new regime.

The S&P 500 remains “tactically” bullish, wherein risk added would require strict targets and exit levels to avoid behavioral biases from exaggerating mistakes when markets turn volatile.

KYLE TAN, MSFE, CSS is a Portfolio Manager at Metrobank’s Trust Banking Group, managing the bank’s offshore Unit Investment Trust Funds (UITF). He holds a Master’s degree in Financial Engineering from the De La Salle University, a Level 3 candidate of the Chartered Market Technician (CMT) certification course and a PSE Certified Securities Specialist (CSS). He spends his free time working out, training at the gun range, or hunting for rare Star Wars collectibles.