Peak inflation: Are we there yet?

You probably think that inflation is now easing, given the latest inflation data.

Not necessarily. The minor 0.1% relief posted by Philippine inflation in August was driven by the slower acceleration of transport costs arising from lower gasoline and diesel prices, as global oil prices declined amid recession concerns fueled by high US inflation prints and the slow economic recovery of China. This was also due to curtailed growth in the prices of food and non-alcoholic beverages since prices of meat, fish, and vegetables declined.

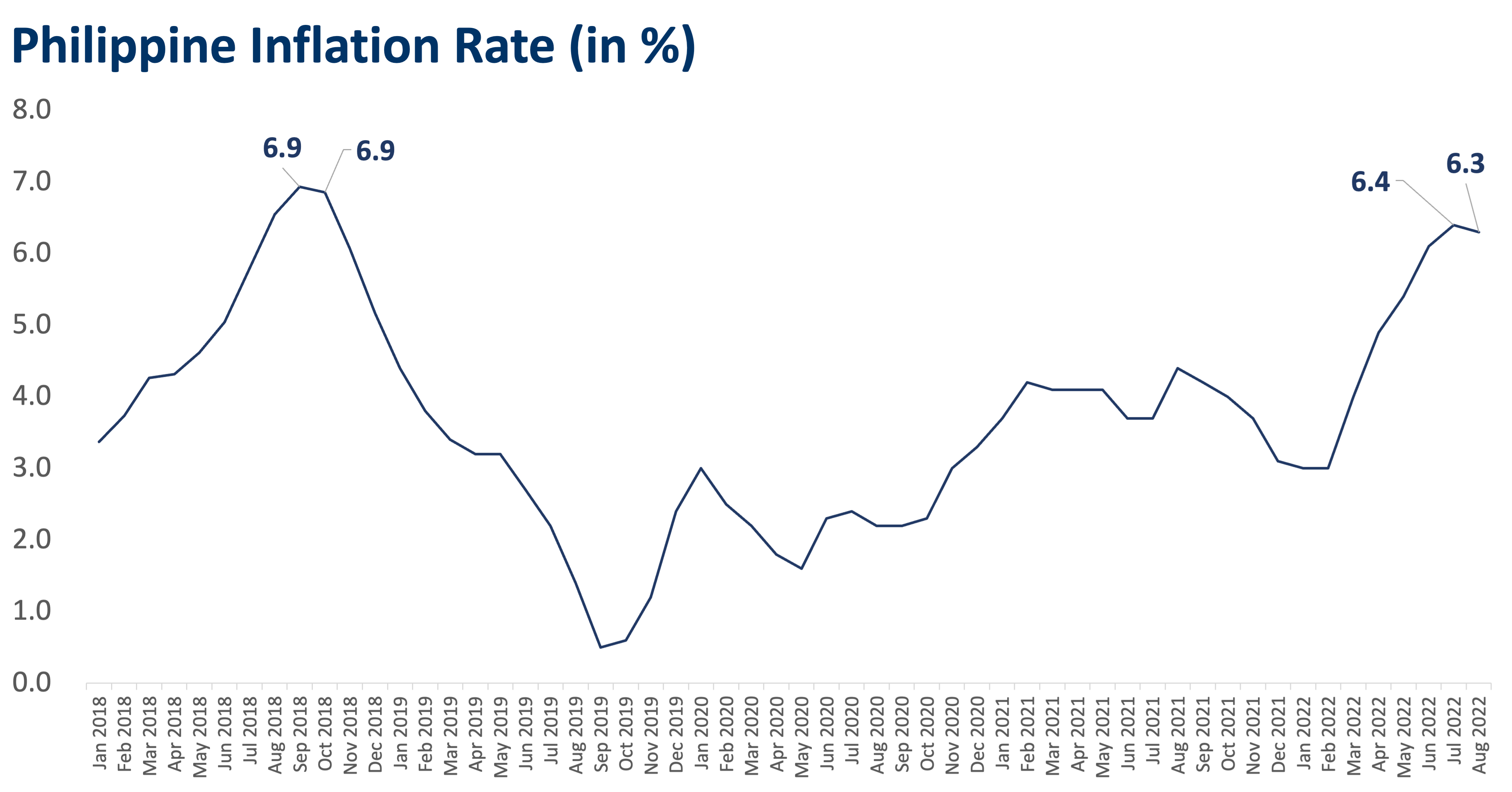

August’s 6.3% inflation rate was only a tad bit lower than the prior month’s 6.4%, which was the highest in around four years, or since October 2018.

However, hold that sigh of relief. It is unlikely that inflation has already peaked. For one, only three out of 12 commodity groups actually had a slower acceleration in prices in August. The other nine (i.e., alcoholic beverages and tobacco, clothing and footwear, etc.) posted higher inflation rates.

In addition, second-round effects (which we wrote about here) are expected to drive inflation even higher. Minimum wage hikes were enforced in 14 regions all over the Philippines last June 2022, and some are to be implemented in tranches until January 2023. Another jeepney fare hike is also due this September, apart from the hike implemented in July. These effects are seen to further add to inflationary pressures in the coming months.

Moreover, continued hawkish signals from the Federal Reserve may further contribute to peso depreciation. The peso hit the PHP 57 level in early September. If the local currency continues to weaken, this will result in costlier imports, which will substantially contribute to inflation since the Philippines is an import-dependent country.

On top of this, the Philippines has been experiencing supply shortages in certain food commodities (e.g., salt, sugar, and onions) due to various structural complications and harsh weather, prompting the need to increase imports. A depreciated peso and a shortage in supply that raises import dependence are a bad combination and may thrust inflation upwards.

Note that a further decline in global oil prices may help alleviate inflation in the second half of 2022, amid renewed recession and diminished demand concerns in the US, as the Fed is seen to maintain or be even more aggressive in its rate hikes given high US inflation prints for August. However, this may be offset by a cold winter in the northern hemisphere accompanied by limited energy supply sources, which may push energy prices up.

The Organization of Petroleum Exporting Countries (OPEC) also stuck to its global oil demand forecast of an increase of 3.1 million barrels per day in 2022, despite concerns of a recession and lower demand. This has recently rallied oil prices.

Thus, we expect Philippine inflation to peak at around the 4th quarter of the year, driven by second-round effects passing on to food, transport, and other non-energy commodities, and aggressive Fed rate action which may lead to currency depreciation. Continued energy supply constraints, especially during the winter season, may also push energy prices up, which will likely cascade to the Philippines.

As the Department of Trade and Industry (DTI) said, “stock up on your Noche Buena items”. Inflation is probably here to stay.

ANNA ISABELLE “BEA” LEJANO is a Research & Business Analytics Officer at Metrobank, in charge of the bank’s research on the macroeconomy and the banking industry. She obtained her Bachelor’s degree in Business Economics from the University of the Philippines School of Economics and is currently taking up her Master’s in Economics degree at the Ateneo de Manila University. She cannot function without coffee.