Under the swap lines program, a partner central bank may sell its local currency to the US Fed to purchase US dollars at the prevailing exchange rate. The two institutions then promise to exchange the currencies again after seven days.

This allows the partner central bank to lend the dollars to banks in its respective country that are in dire need of dollar funding. While the Fed is not allowed to lend or invest the foreign currency holdings, it is still compensated by being paid the interest earned on the partner central bank’s dollar loan.

For traders and investors engaged in the USD/PHP forex market, awareness of such swap lines and central bank activities is crucial. These interventions can impact the supply and demand dynamics of US dollars, potentially influencing the exchange rate between the dollar and the peso. Monitoring these developments provides insights into the liquidity conditions and can be considered when assessing forex opportunities in the dollar-peso pair.

The first swap lines were established in December 2007. Initially limited to the Fed, European Central Bank (ECB), and Swiss National Bank (SNB), the swap lines were meant to address a shortage in US dollar funding, as financial institutions were heavily invested in mortgage-backed securities (MBS) – bonds that derived principal and interest payments from US housing loans.

Believing that the US housing market would continue to appreciate, mortgage lenders were aggressively offering loans to borrowers with low income and creditworthiness also known as “sub-prime.”

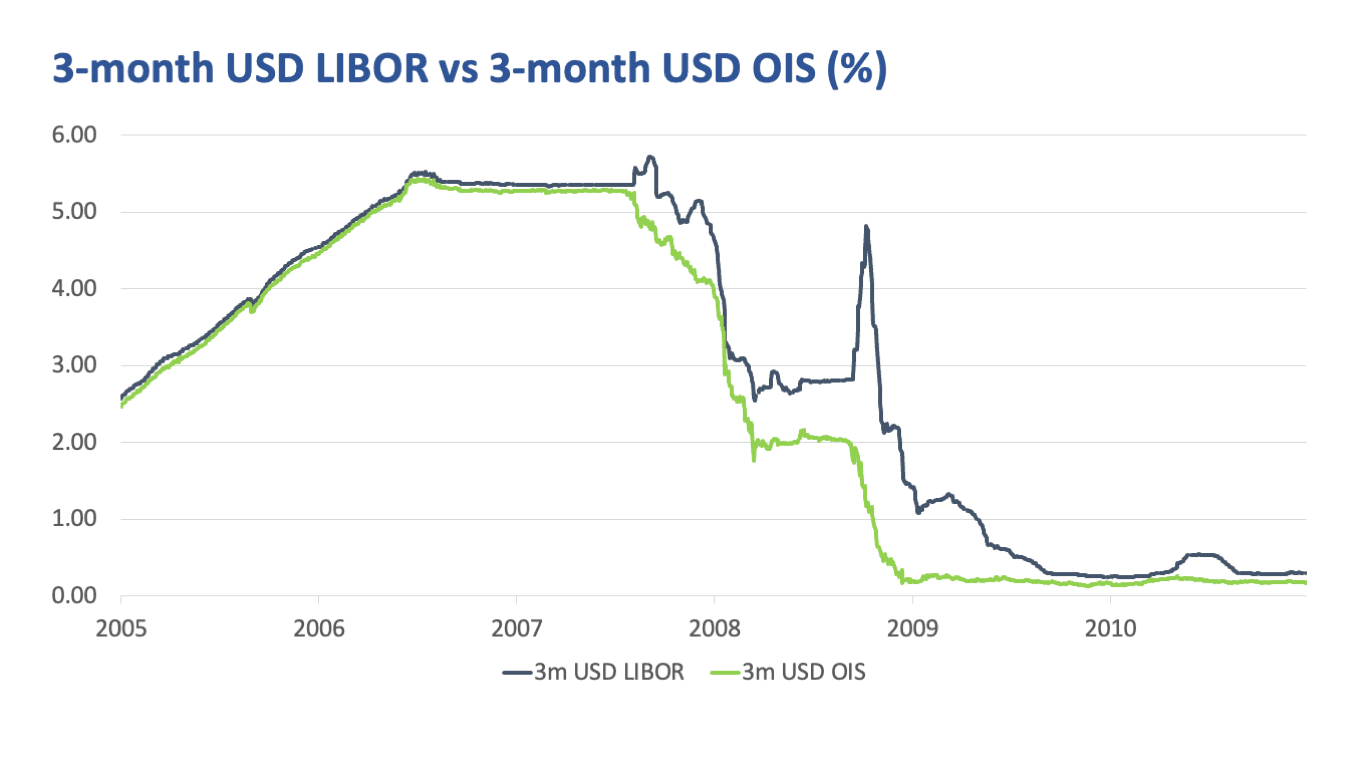

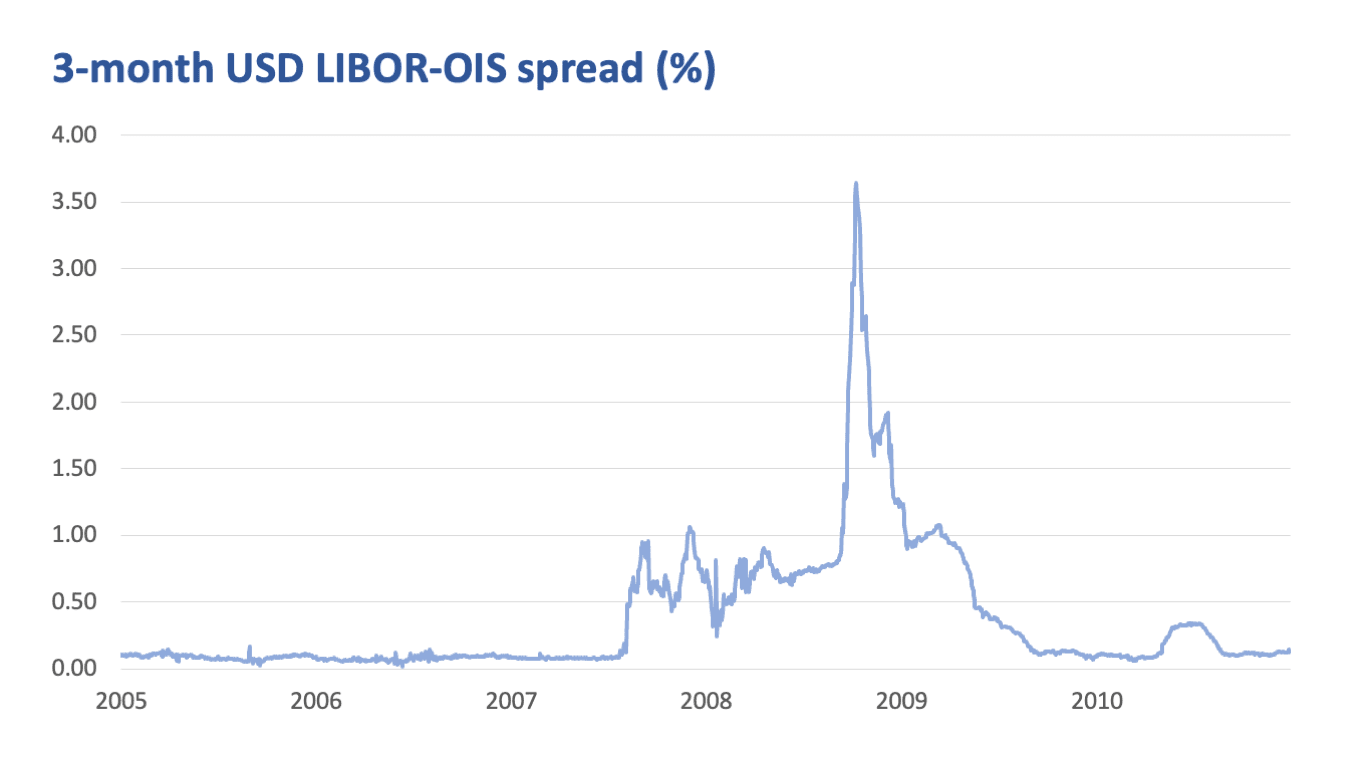

Eventually, these underlying sub-prime mortgages started to fail, which also caused the bonds to become worthless. Global banks suddenly found themselves scrambling for cash, specifically US dollars. This was the beginning of the global financial crisis (GFC).