Currencies5 MIN READ

Why USD/PHP is at levels never seen before

Explore what is driving the movements in the local currency.

June 19, 2026 by Anna Cudia

Share this article:

Foreign exchange (FX) movements are best viewed as outcomes of broader macroeconomic forces rather than signals in isolation. Because FX always reflects the interaction between two currencies, it provides insight into relative growth trends, policy stance, and risk sentiment across economies.

Currencies respond to a mix of interest‑rate policy, capital flows, trade dynamics, and investor confidence. Central bank actions—whether actual rate moves, direct intervention, or even guidance—can influence currencies by shaping expectations and short‑term liquidity conditions. Recent policy signals in parts of Asia highlight how credibility and timing often matter as much as the level of rates.

Growth patterns also play a role. Rapid expansion in net‑importing economies can widen trade deficits, increasing demand for foreign currency. In contrast, strong growth in net‑exporting countries is more likely to generate foreign‑currency inflows. Political uncertainty tends to weaken currencies as foreign capital becomes more selective, while stable governance and policy credibility can help anchor exchange rates.

At a structural level, balance‑of‑payments flows are critical. Elevated oil prices tend to pressure the currencies of energy‑importing countries through higher import bills, while foreign portfolio and direct investments, as well as remittances, can provide support by boosting foreign‑currency inflows.

For instance, inclusion in a global bond or equity index can drive pre‑positioning by foreign investors ahead of actual implementation, increasing demand for the local currency and leading to appreciation. However, such gains tend to unwind quickly during global risk‑off shocks, such as the Middle East conflict.

Recent Middle East tensions have reinforced broad US dollar strength, reflecting heightened risk aversion and the dollar’s role as a global safe haven. While several Middle Eastern currencies are pegged to the US dollar, the key transmission channel into Asia is commodity pricing and capital flows rather than exchange‑rate regimes themselves.

With higher oil prices and the petrodollar dynamics, i.e., petroleum typically being paid in dollars, net oil importers will need to buy more dollars for the same volume of oil they need.

For many Asian economies, dependence on Middle East energy imports means higher oil prices translate into greater demand for US dollars and wider trade pressures.

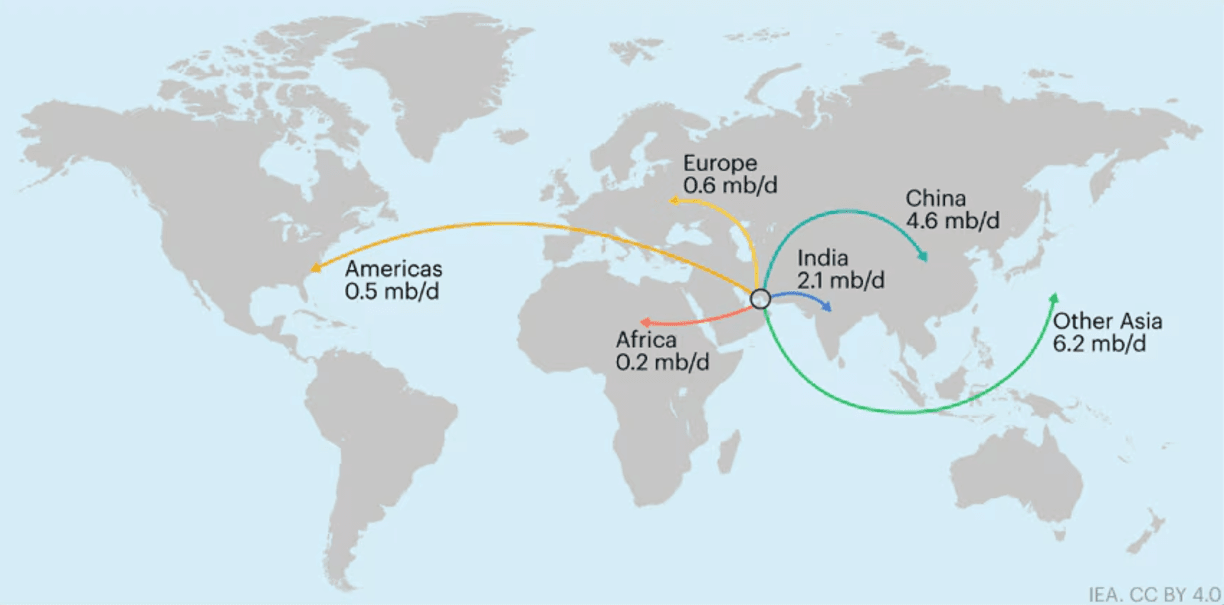

This shows crude oil exports transiting the Strait of Hormuz by destination in million barrels per day (2025). Total does not match sum of adding individual numbers due to destinations not indicated. Source: International Energy Agency

Within ASEAN, the Philippine peso’s sensitivity to oil prices is most comparable to the Thai baht and Vietnamese dong, while differences relative to the Indonesian rupiah highlight how commodity exports can partially offset energy shocks. In relative terms, the peso has underperformed regional peers during the first two months following the escalation of Middle East tensions in late February 2026.

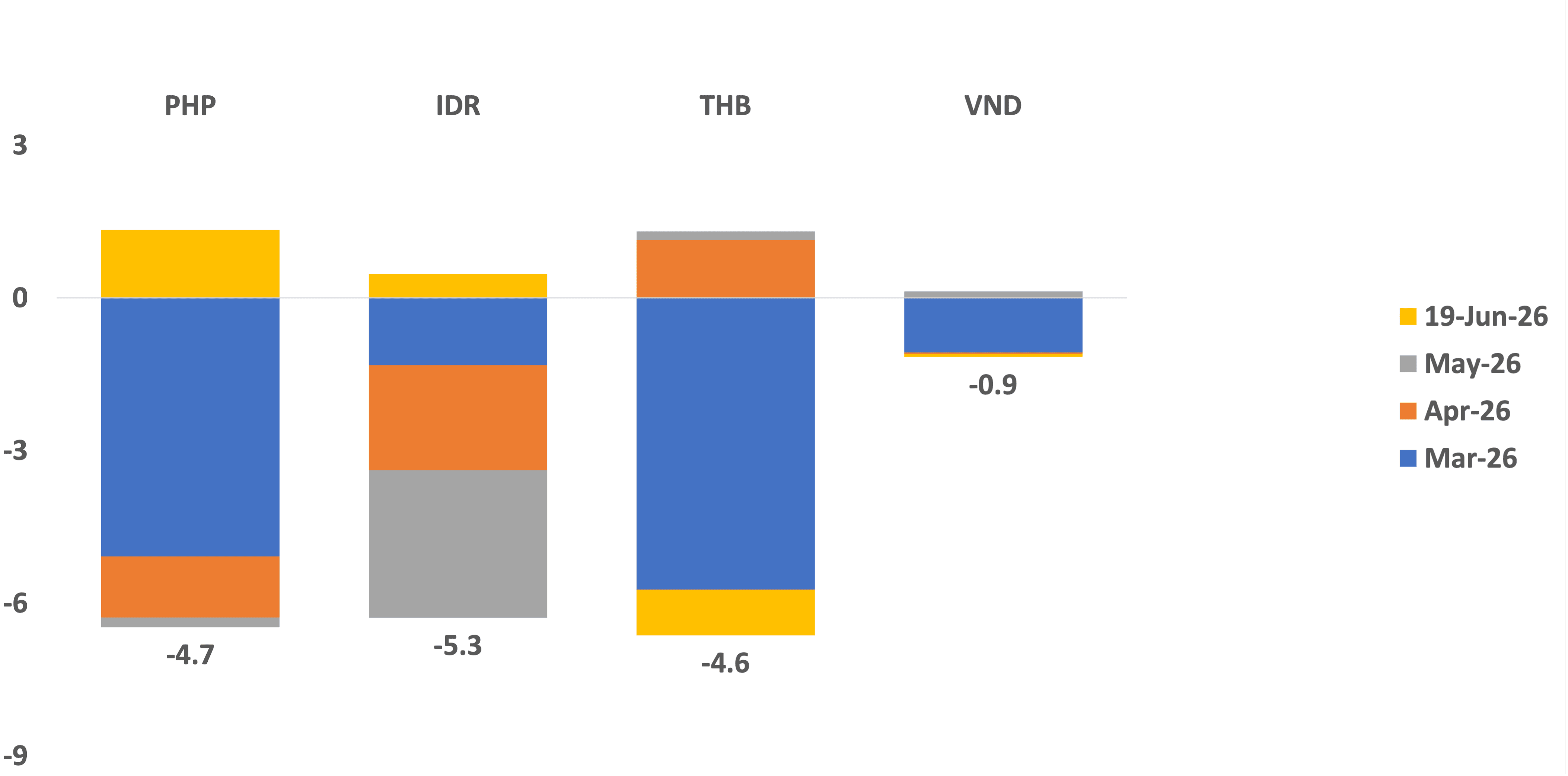

This shows the month-on-month performance of Asian currencies since February 2026 (%). Source: Bloomberg

Despite shared external pressures, inflation outcomes differ. Higher oil prices have fed into inflation most clearly in the Philippines, been more contained in Thailand, and more limited in Indonesia and Vietnam due to subsidies and administered pricing. These differences reflect variations in CPI composition and price pass‑through. For FX, this matters because it shapes policy flexibility and perceptions of relative currency resilience.

Note: Change in average inflation over March-May 2026 versus February 2026 in percentage points. Sources: International Trade Centre, Bangko Sentral ng Pilipinas, Philippine Statistics Authority, State Bank of Vietnam, Vietnam National Statistics Office, Bank of Thailand, Thailand Trade Policy and Strategy Office, Bank Indonesia, BPS-Statistics Indonesia, Metrobank Research estimates

Not all peso moves are US‑dollar stories. The exchange rate reflects a balance between global forces and domestic fundamentals. Structural supports include remittances from overseas Filipinos and services exports, particularly from BPO activities, which provide steady foreign‑currency inflows.

At the same time, the Philippines’ status as a net importer—especially of energy and key food items—creates recurring demand for foreign currency. Seasonal patterns also matter, with the peso often facing pressure when import demand rises ahead of the year‑end period. Policy credibility and the broader investment climate remain important in influencing capital flows over time.

The peso is seasonally weak in the third quarter and strong in the fourth quarter of the year. Figures reflect the average change in USD/PHP per quarter, i.e., if the USD/PHP goes higher, the figure is positive. Meanwhile, colors refer to peso appreciation (green) or depreciation (red) against the US dollar. Source: Bloomberg

Sometimes it is about the peso, other times it is about the dollar. Sources: Bloomberg, Metrobank Research

Potentially supportive: Peso weakness can benefit goods and services exporters and foreign‑currency earners through favorable earnings translation, particularly where cost bases are largely peso‑denominated. Sectors such as BPOs, IT services, exporters, and firms with dollar revenues but peso costs may see margin support.

Areas of pressure: Import‑dependent firms face higher FX‑driven input and fuel costs, weighing on margins and earnings visibility. Airlines, logistics firms, manufacturing, and energy‑intensive industries, as well as companies with foreign‑currency liabilities, may experience increased strain on cost structures and cash‑flow planning during periods of peso weakness.

FX does not move in isolation. Peso dynamics reflect both global conditions and domestic fundamentals. For investors, understanding these drivers helps put currency moves into context—where interpretation matters more than timing.

FX trends can meaningfully influence investment outcomes by amplifying or moderating underlying asset returns. In volatile macro environments, relative currency movements become increasingly important when assessing cross‑market exposures.

While FX hedging provides some comfort by reducing currency uncertainty, total investment returns ultimately matter most. In this context, high investment returns may be less attractive if the currency is highly volatile, as asset prices typically move with the country’s risk‑return dynamics.

Related Article: How to manage peso weakness through hedging

ANNA DOMINIQUE CUDIA, MBA, CSS, oversees Metrobank’s Macro Research Department, steering macroeconomic and financial market analyses for clients. She previously led the Markets Research Department of Metrobank’s Trust Banking Group and was part of Investor Relations, supporting multi-billion peso and US dollar capital-raising initiatives. She holds an MBA in Finance, with distinction, from the University of London, and industry certifications in finance. Outside of work, she enjoys travel and exploring new perspectives.