A daily dose of market updates to guide your investment decisions.

August 4, 2026

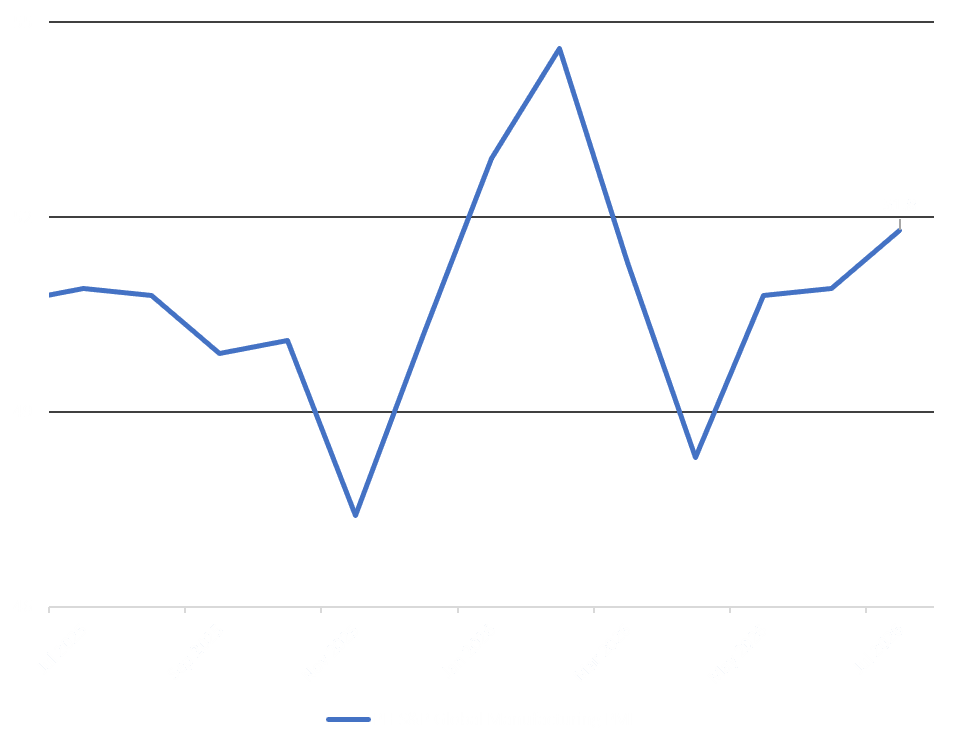

Chart of the Day

Philippine manufacturing activity expanded for a third consecutive month, with the Purchasing Managers’ Index (PMI) rising to 51.8 in July from 50.9 in June. The expansion was driven by stronger customer demand, higher new orders, fresh business opportunities, and increased production, supporting sector growth. Meanwhile, rising input costs, partly attributed to the Middle East conflict, intensified inflationary pressures and led firms to increase selling prices. Sources: Bloomberg, S&P Global

Financial market updates

The USD/PHP exchange rate opened 24 centavos lower at 61.00 on Monday, and the volatile morning saw the pair reach highs of 61.08 and then bounce from 60.95.

The pair saw better balance around 61.00-61.04 for most of the morning as corporate demand accumulated at these relatively low levels.

However, strong selling interest from offshore counterparties dragged the pair lower, touching intraday lows of 60.87.

The USD/PHP pair ultimately closed at 60.93, or 31 centavos lower day-on-day.

The current support levels of USD/PHP remain at 60.60/85, while the resistance levels are 61.05/25.

Local bonds extended gains on fresh prospects for US-Iran negotiations, easing oil prices, and a lower USD/PHP exchange rate. Monday’s Treasury Bill auctions saw strong demand, with average awarded yields down 2-4 basis points (bps).

Belly bonds rallied, led by the 3-Year benchmark FXTN 7-68, which closed 10 bps lower at 7.000%. Spillover demand pulled 4-Year bond yields 5 to 7 bps lower, between 7.120% and 7.150%, while the 6- to 8-Year bonds saw buying at 7.300%.

Decent participation is expected at today’s 5-year FXTN 20-17 auction, with an updated indicative range of 7.150% to 7.250%.

Markets await the July Philippine Inflation report, due on August 5, with Metrobank’s headline forecast at 6.5%, driven by high oil prices and a weaker peso. Middle East headlines remain a concern as well.

The Philippine Stock Exchange index (PSEi) ended 98.28 points higher at 6,334.72 on Monday as investors rotated back into large names after last week's month-end weakness.

Investors drew confidence from a steadier regional backdrop and focused on accumulating core names ahead of the week’s earnings releases and macroeconomic data.

Market breadth remained healthy, with 109 advancers against 79 decliners on PHP 5.10 billion value turnover, even as foreign investors posted a modest net inflow of PHP 75.66 million.

The International Container Terminal Services Inc. (+72.29 points) did the heavy lifting, with solid support from the Bank of the Philippine Islands (+9.98 points), BDO Unibank Inc. (+5.89 points), and SM Prime Holdings Inc. (+4.60 points).

Meanwhile, leading the drag on the index were Ayala Land Inc. (-9.67 points), AREIT Inc. (-1.71 points), RL Commercial REIT Inc. (-1.64%) and San Miguel Corp. (-1.64%).

The report above is circulated for general information only. The opinions expressed are solely those of the contributors and are based on prevailing market conditions and public sources that are believed to be reliable. Metrobank and the report contributors/support staff do not make any guarantees or representation as to the accuracy, completeness or suitability of this report.

The report may contain confidential or legally privileged material and may not be copied, reshared, redistributed, or published without prior written consent. Opinions or strategies contained in this publication may change without prior notice and should not take the place of professional investment advice or sound judgment on the part of the reader.