Rates & Bonds3 MIN READ

Will the government issue retail treasury bonds soon?

Here’s what to expect in Philippine fixed income markets in the second half of the year

June 24, 2026 by Anna Cudia

Share this article:

Local government bond yields recently experienced unusually large swings following the US-Iran Memorandum of Understanding and the sharp decline in oil prices.

However, recent market optimism may be running ahead of developments on the ground, as a final peace agreement has yet to be reached and geopolitical risks remain. While lower oil prices could reduce some inflation pressure, a final peace agreement is not yet in place.

Related Article: Why oil prices may ease—but normalize more slowly than expected

Even with its recent deceleration, Philippine inflation in May 2026 printed at 6.8%, remaining well above the Bangko Sentral ng Pilipinas’ (BSP) target range of 3±1%.

Related Article: Inflation Update: Lower than expected

Inflation is unlikely to return immediately to pre-conflict levels as oil prices may normalize only gradually, while second-round effects and peso weakness continue to pose upside risks.

In its recent monetary policy meeting, the Monetary Board decided to increase policy rates by 25 basis points (bps) again, as anticipated by the markets.

Related Article: BSP Update: Persistent inflation prompts rate hike

The BSP also expects inflation to remain above target through 2027, reinforcing expectations that policy rates may need to stay restrictive for longer than previously anticipated.

Recent bond rallies reflect improving sentiment, but inflation and policy risks suggest markets may be moving ahead of the underlying fundamentals.

Aside from rates, supply dynamics also matters to fixed income markets. Even if inflation drives the demand story, supply could become the defining theme for local bonds in the second half of the year.

With the National Government continuing to face significant funding requirements, especially with lackluster demand in first half of the year amid the Middle East conflict, supply dynamics may become increasingly important to monitor.

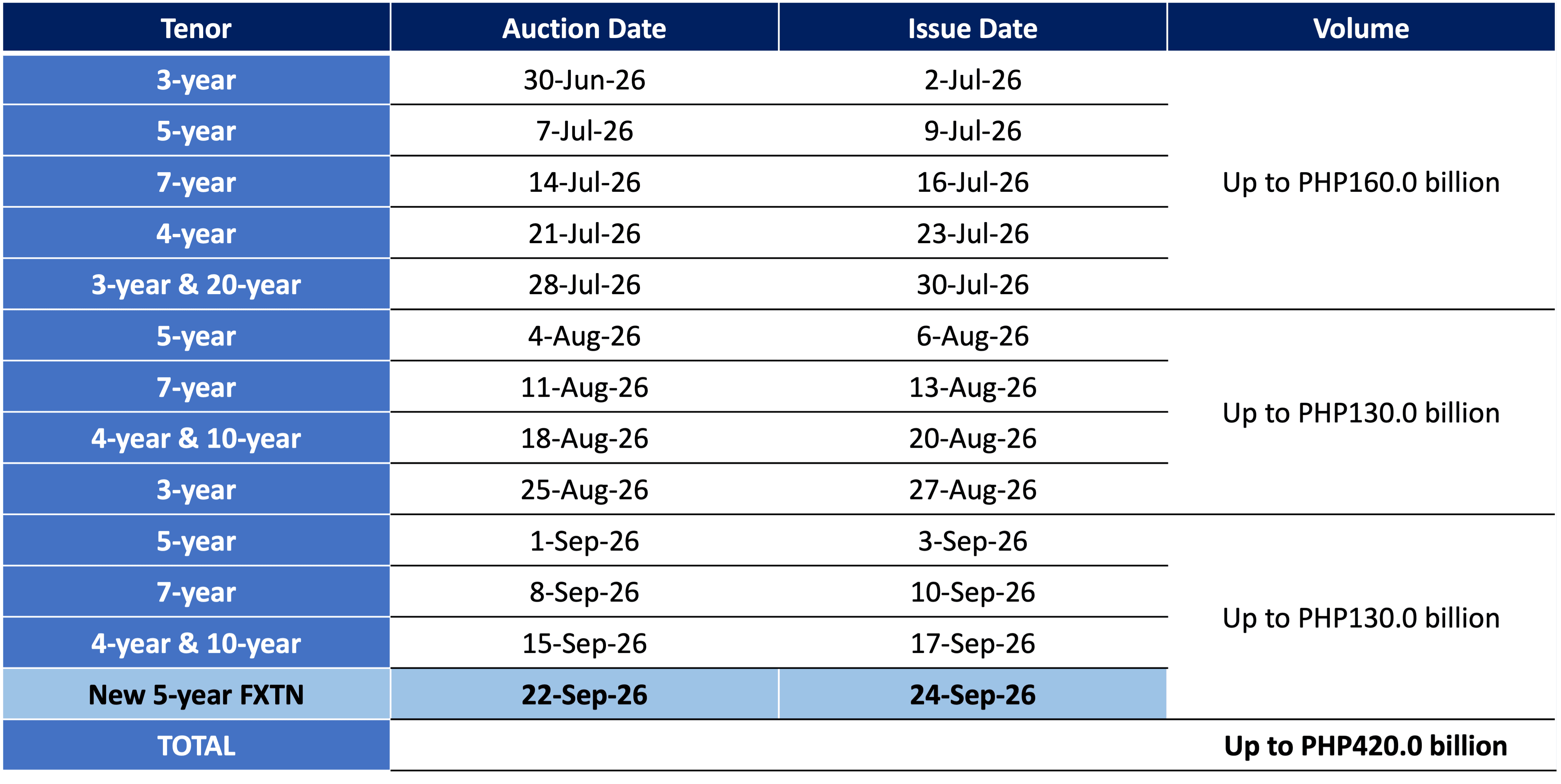

Note: The Bureau of the Treasury (BTr) reserves the right to revise the tenors and total volume to be issued, which will be determined upon the release of the Notice of Public Offering in the days leading up to the auction date. Source: Bureau of the Treasury.

The government has already returned to offshore markets through dollar bond issuances and continues to maintain an active domestic funding program. As bond yields have declined, funding conditions have become more favorable for issuers such as the National Government.

Finance Secretary Frederick Go recently mentioned that the government may issue Retail Treasury Bonds (RTBs) in the second half of 2026, subject to market conditions and funding requirements.

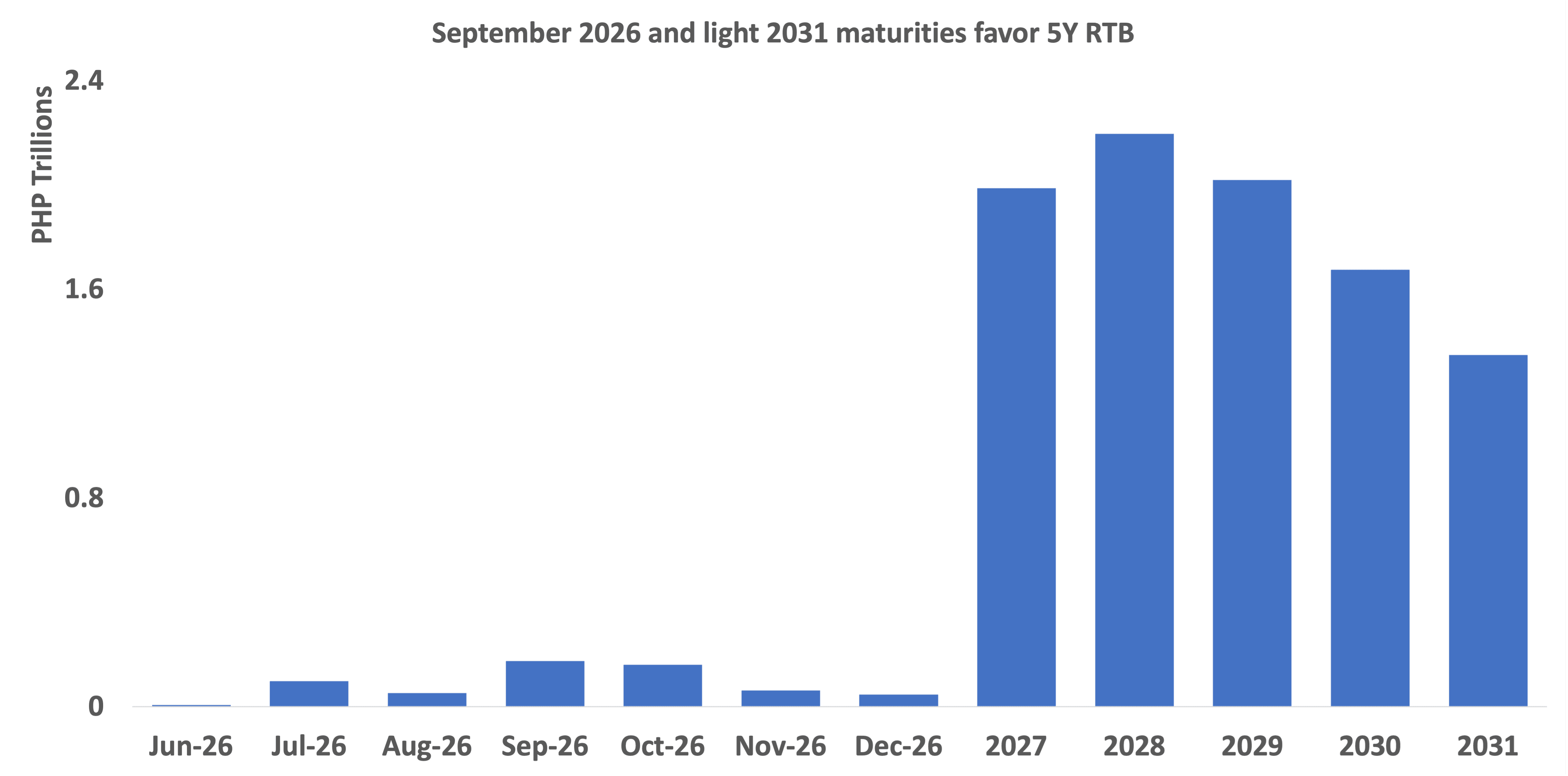

RTBs remain one of the government's most important retail funding tools. Beyond the coupon itself, the eventual tenor may provide an important signal about where authorities see funding efficiency and investor demand. Recent RTB issuances have clustered around the 5-year area of the curve, including the 5-year RTB issued in 2025.

With remaining 5-year borrowing needs and relatively light 2031 maturities versus 2027–2031, investors may watch the 5-year segment as a potential reference point, pending final tenor.

Historically, RTBs have often been issued ahead of sizable maturities, making the August-to-September period one area investors may monitor, although no definite timetable has been announced. A sizable issuance could temporarily absorb liquidity and influence pricing across neighboring maturities.

Source: Bloomberg

While there is a lot going on globally, investors may have to look more at what is happening domestically.

First, inflation trajectory says a lot about where interest rates and bond yields can go. Second, BSP’s recent pronouncements and policy signals can influence market confidence and investor expectations. Third, government borrowing through bonds is also something that can move bond yields, especially during times wherein market expectations are far from actual.

In an environment where interest rates are likely to stay elevated for longer, total returns may increasingly depend on carry, or regular interest payments on bonds, rather than expectations of rapid capital gains from falling yields.

Philippine bonds are increasingly being shaped by two competing forces: optimism from lower oil prices and improving market sentiment on one hand, and caution from still-elevated inflation and continuing government financing needs on the other.

ANNA DOMINIQUE CUDIA, MBA, CSS, oversees Metrobank’s Macro Research Department, steering macroeconomic and financial market analyses for clients. She previously led the Markets Research Department of Metrobank’s Trust Banking Group and was part of Investor Relations, supporting multi-billion peso and US dollar capital-raising initiatives. She holds an MBA in Finance, with distinction, from the University of London, and industry certifications in finance. Outside of work, she enjoys travel and exploring new perspectives.