DOWNLOAD

DOWNLOAD

Peso GS Weekly: Expect poor risk-taking appetite and hawkish BSP

Yields of government securities may continue to drift higher in the near-term with the absence of meaningful catalysts.

By Geraldine Wambangco, Metrobank Government Securities Trading Department

By Geraldine Wambangco, Metrobank Government Securities Trading Department

WHAT HAPPENED LAST WEEK

It was a muted start in the peso government securities (GS) market last week as players remained on the sidelines given the current risk backdrop of higher yields and supply risk especially in longer-term bonds.

The Bureau of the Treasury (BTr) was able to fully award the 7-year auction for Fixed Rate Treasury Note (FXTN) 7-71 towards the higher-end of market expectations at an average of 6.299% and a high of 6.35%. The weak auction participation, which only garnered around PHP 46 billion in tenders, led to further defensiveness in the local bonds market. Risk-appetite soured even more with the move higher in global yields.

Retail Treasury Bond (RTB) 5-18 traded to as high as 6.275%, while 10-year bonds were sold up to 6.40%. Longer-tenored peso GS also saw sizeable selling interest to reduce duration.

To end the week, the March inflation data came out at 3.7% vs. 3.8% consensus estimates, but failed to boost risk-taking appetite.

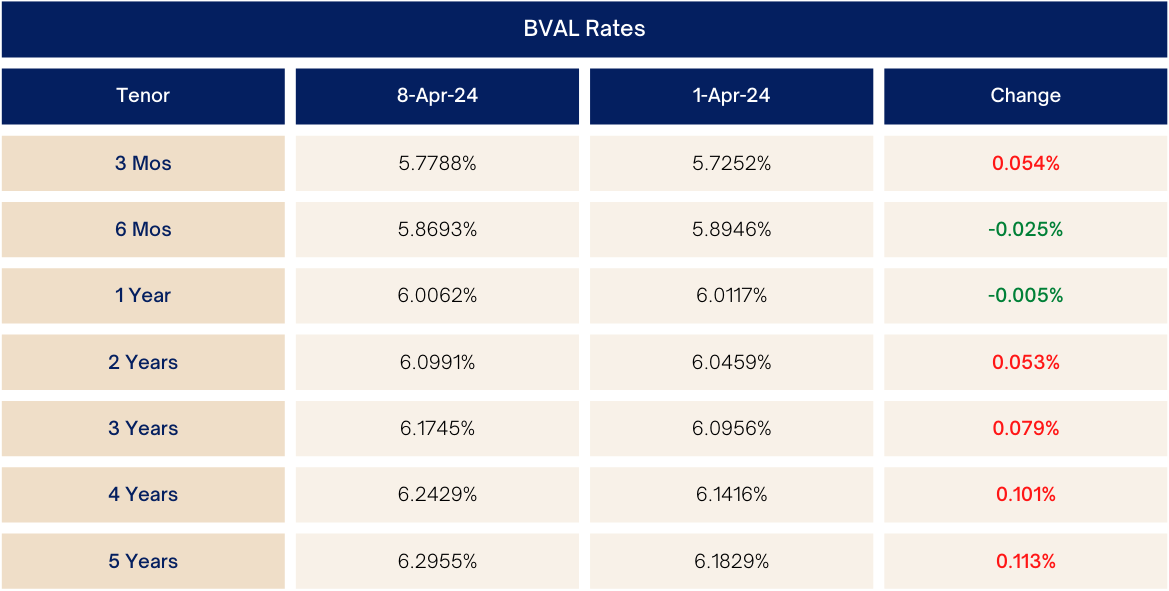

Market Levels (week-on-week)

WHAT WE CAN EXPECT

Bangko Sentral ng Pilipinas (BSP) Governor Eli Remolona, Jr., also had a hawkish tilt in his statements and mentioned that inflation risks have increased. With the absence of meaningful catalysts that could help improve market sentiment, the same defensiveness is likely to be seen in the GS space and yields may continue to drift higher in the near-term.

For next week’s 15-year auction, the Bureau of the Treasury (BTr) will be reissuing Fixed Rate Treasury Note (FXTN) 20-23, where our early indicative range stands at 6.70-6.90%. The market will also continue to monitor the behavior of the BTr in the upcoming auctions given if it will continue to award at higher levels.

A rejection of the auction, on the other hand, is likely to provide some reprieve for local bonds. At current levels, we see value in the 5-year benchmark bond, RTB 5-18 near the 6.60-6.65% area given the absence of supply risk in this tenor for the remainder of the second quarter.

See our top picks below:

Note: Rates are indicative and subject to refresh.