Does the BSP need to keep up with the Fed?

To curb inflation, central banks raise interest rates to reduce the amount of money circulating in the economy and increase the cost of borrowing. This then makes people borrow less and spend less, reducing economic activity that helps cool down an overheating economy, i.e., cooling down demand inflation.

In light of this, the US Federal Reserve (Fed) used contractionary monetary policy to hike the Fed funds rate by 75 basis points (or 0.75 percent) to a range of 1.5% to 1.75% this June, its biggest rate hike since 1994. This is in response to the staggering 8.6% US inflation rate in May 2022, the highest since December 1981.

Compared to the Philippines, which experienced 5.4% inflation in May 2022, the Bangko Sentral ng Pilipinas (BSP) has so far hiked key rates (called overnight repurchase or RRP rates) by 50 basis points – 25 bps in May and another 25 bps in June – to bring the RRP rate to 2.50%. With more aggressive Fed rate hikes expected, is there a need for the BSP to also hike rates aggressively in the coming months?

Inflation in the Philippines is more food-driven than in the US; that is, the former’s food commodities have a higher weight in its Consumer Price Index (CPI) at 34.8% vs. the 13.37% for the US CPI. Additionally, the Philippines is highly dependent on food imports compared to the US.

For example, rice is around 9% of the CPI basket and there is heavy dependence on rice imports to keep supplies up and help keep prices down. Food inflation is therefore more critical for the Philippines than for the US.

On the other hand, US inflation is more energy-driven than the Philippines’, particularly now. This is because President Joe Biden reversed US energy policies in 2021 to tackle climate change. Before that, the US was a major oil exporter and could swing prices in global oil markets. But with the policy reversal, it eventually ended up being a price-taker, with the resultant high fuel prices, especially as the sanctions against Russia started to bite.

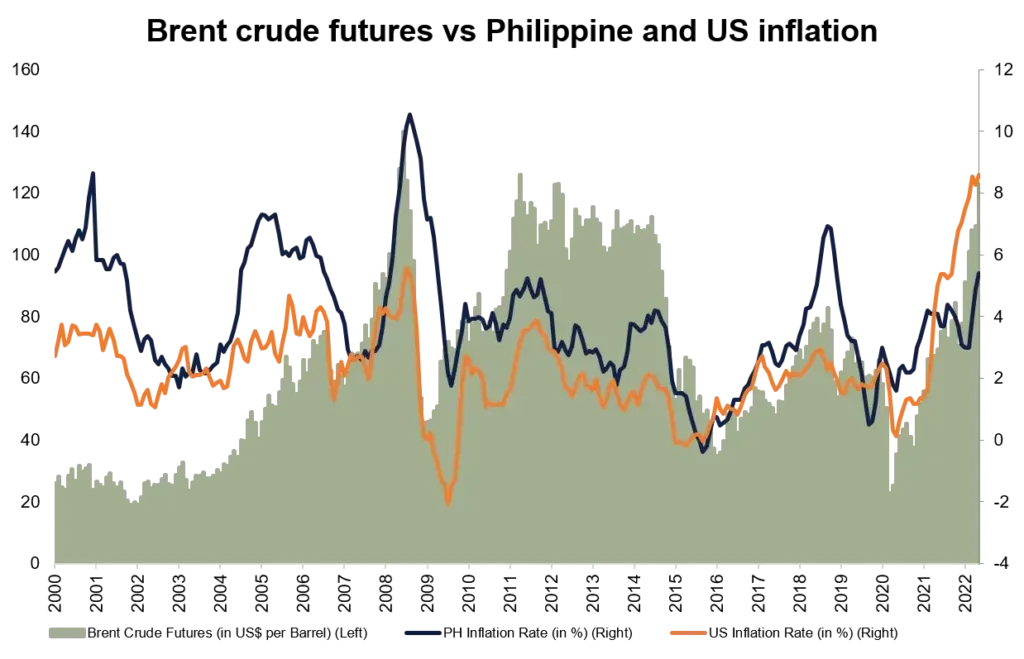

Taking a look at the chart, one can see that since 2021, a rise in the price of Brent crude has led to a dramatic increase in US inflation, way more than Philippine inflation. In previous episodes, Philippine inflation rose dramatically, well above the US inflation rate when Brent prices were peaking in 2008, between 2010-2014, and in 2018.

But this time around, US inflation has shot up way beyond Philippine inflation and it appears to still be upward bound as Brent started hitting USD 120 a barrel. The Philippines, on the other hand, is currently seeing inflation similar to 2011 conditions when Brent was peaking around the USD 120 levels as well, although of course there is also an upward bias.

Turmoil in the oil markets pushed US inflation far higher than it did Philippine inflation. That’s because US energy policies shifted their focus on renewable energy in 2021, when the thought of Russia invading Ukraine was considered highly unlikely.

The key takeaway here is that the US is now more vulnerable to energy prices peaking as proxied by Brent, and with inflation hitting past the 8% level and threatening to go double-digits, it is not surprising to see the Fed signaling very aggressive rate hikes on top of its recent hikes as it tries to tackle inflation.

For the Philippines, on the other hand, the situation resembles 2011 in terms of Brent oil and inflation rates, with an upward bias but still relatively tame compared to US inflation. It thus begs the question if aggressive rate hikes are warranted right now as they are for the US.

Of course, rate hikes are in the cards, which is why the BSP has been hiking rates and has signaled more rate hikes in the future. Clearly, however, there is no need to move in lockstep with the US Fed, if this chart is any indication.

ANNA ISABELLE “BEA” LEJANO is a Research & Business Analytics Officer at Metrobank, in charge of the bank’s research on the macroeconomy and the banking industry. She obtained her Bachelor’s degree in Business Economics from the University of the Philippines School of Economics and is currently taking up her Master’s in Economics degree at the Ateneo de Manila University. She cannot function without coffee.