Understanding debt: Why the Philippines is not Sri Lanka

Much has been said about the 63% debt-to-GDP ratio of the Philippines, that it is supposedly “beyond the 60% debt threshold” set as some sort of international benchmark. However, there is no such thing as an established debt threshold above which an economy will likely start collapsing.

In fact, there are arbitrary debt thresholds set at different levels by different entities that have no common basis with any idea that breaching such threshold would mean economic collapse. Yes, thresholds are set, but these are arbitrary and only relevant to an end in mind. It does not mean doom and gloom.

For example, to be part of the Euro zone at the onset, European countries that wanted to ditch their currencies (deutschmark, francs, etc.) in favor of the euro had to fix their debt-to-GDP ratio at a 60% ceiling, among other things, before monetary union could be established. It did not mean that these economies would collapse with debt beyond the 60% ceiling set, as this only meant that they could not join the Euro zone.

However, there is one kind of debt that is dangerous if unmanaged, and that is foreign currency debt, here simplified as dollar debt for ease of discussion. The country cannot create its own dollars, so it will have to rely on dollar revenues to pay for any dollar debt incurred. Of course, it can always buy dollars in the market or borrow even more dollars to pay for dollar debt that is falling due.

This is very different from domestic or peso debt, as the country can always “print” more pesos to pay for peso debt, the peso being the home currency of the country. For example, US debt is more than 100% of its GDP, while Japan’s debt is more than 200% of its GDP. However, it is not problematic per se for these countries as their debt is denominated in their respective home currencies – the dollar and yen.

So clearly, breaching a 60% debt-to-GDP ratio is a non-event as the more pressing issue is about how much is the dollar debt and how much are the assets (called Gross International Reserves or GIR) backing up the debt, to simplify things. More to the point, the total amount of dollar debt that falls due in the short term versus how much dollar assets or GIR the country has on hand is the more critical issue.

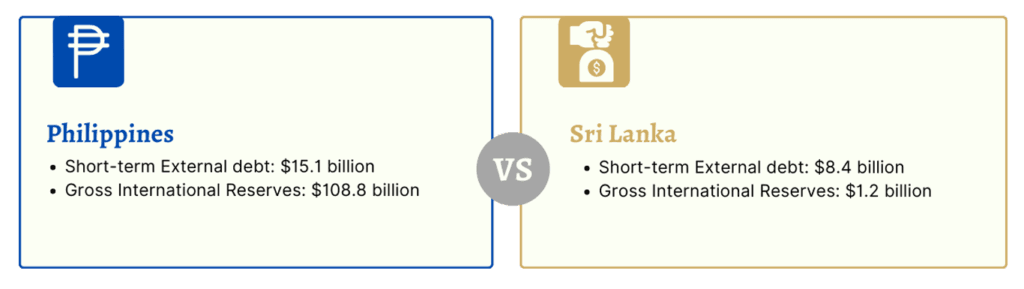

Let’s now compare the Philippines vs. Sri Lanka as of yearend 2021:

Clearly, the Philippines is in no way near the situation of Sri Lanka. The latter has USD 8.4 billion to pay in the short term and it has only USD 1.2 billion in dollar reserves, so it must borrow dollars to pay its dollar debt in a classic Balance-of-Payment (BOP) crisis. The Philippines, on the other hand, can pay all its dollar debt of USD 106 billion with its USD 108.8 billion in dollar reserves, but that’s not even the issue. The critical part is only the USD 15.1 billion dollars in short term debt. So, the country can pay all its short-term dollar debt and have spare dollars for continued imports without having to borrow dollars at all.

There are all kinds of indebtedness and the Philippines is not bankrupt at all despite its 63% debt-to-GDP ratio, principally because its debt is manageable and its dollar debt is more than 100% backed up by dollar assets. Clearly, the Philippines is not Sri Lanka.

MARC BAUTISTA, CFA, is Vice-President and Head of Research & Business Analytics at Metrobank, in charge of the Bank’s macroeconomic, industry, and financial market analysis and research. He loves teaching finance and investments, portfolio management, statistics, financial derivatives, economics, etc. in a university setting. He plays guitar in a rock band and also loves learning other languages, especially Spanish, promoting its recovery as a heritage language in the Philippines.