DOWNLOAD

DOWNLOAD

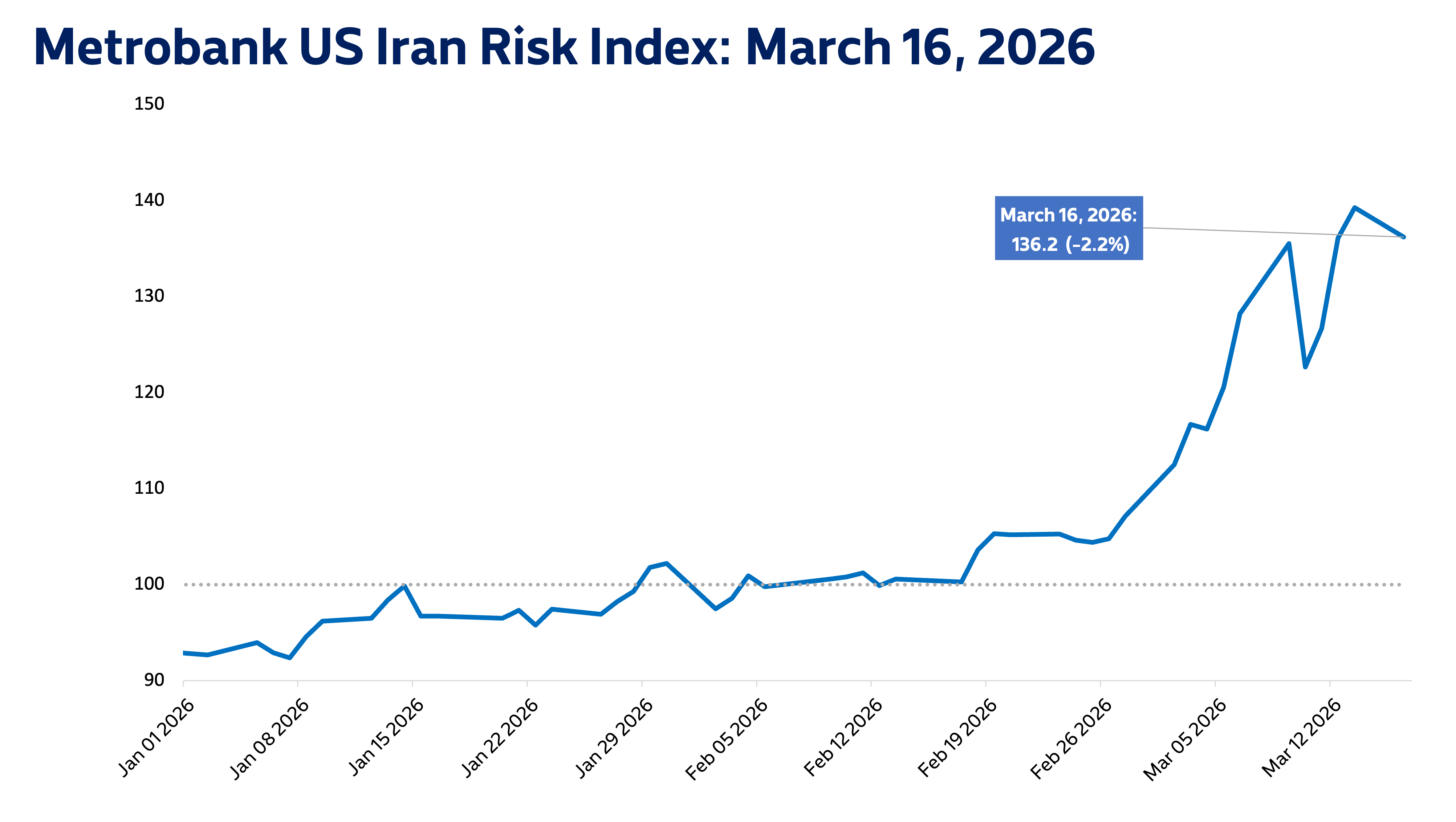

Metrobank US-Iran Risk Index: Safer passage?

While oil prices moved lower overnight, overall supply conditions will still be constricted.

By Metrobank Research, Investment Counselor Department

By Metrobank Research, Investment Counselor Department

Metrobank’s US-Iran Risk Index settled at 136.2 on March 16, 2026, 2.2% lower than the previous day.

Brent crude prices fell overnight following news that some ships and vessels were able to pass through the Strait of Hormuz, a critical passageway for 20% of the world’s oil shipments. According to Reuters, Iran has reportedly allowed some Indian oil tankers to sail through the passage following talks between the two countries.

Financial markets took the news as a momentary source of relief for oil prices. The benchmark 10-year US Treasury yield settled lower on March 16, US trading hours. The US dollar’s strength also softened marginally overnight.

Even with this news, conditions surrounding the Strait of Hormuz remain tight. US President Donald Trump has already reprimanded US allies for failing to assist in escorting oil shipments through the passage. Global oil supply will likely stay constricted as long as military tensions between the US and Iran persist.

We maintain our expectation for upside oil risk to endure, as the Middle East conflict rages on. As domestic inflation accelerates on rising oil prices, we expect the Bangko Sentral ng Pilipinas (BSP) to preemptively end their easing cycle this year. Additionally, dollar strength will persist, as safe-haven demand continues. This puts pressure on the peso and will keep the dollar-peso exchange rate elevated in the near future.

Metrobank’s US-Iran Risk Index measures the amount of risk that the ongoing conflict presents to financial markets. It considers the general risk sentiment of investors and inflationary pressure brought on by the conflict. A value of 100 denotes a normal level of risk based on market levels prior to the conflict’s escalation, while values greater than 100 imply increasing levels of risk.

What now?

| Asset Class | Outlook | Strategy |

|---|---|---|

| Local Fixed Income | Bearish | Stay defensive on duration. Focus on liquid 2–5-year tenors and add only on yield spikes or auction‑driven dislocations. Avoid extending until foreign-exchange and geopolitical risks ease. |

| Local Equities | Bearish | Expect bargain hunting of cheaper names in the near term. However, gains may remain capped amid oil volatility and developments in the Middle East. Buy on dips and take profit in rallies. |

| Global Fixed Income | Bearish | Position in short-dated (up to 5 years) quality bonds, as inflation fears push yields upwards. Expect volatile swings as headlines drive market sentiment amid uncertainty. |

| Global Equities | Neutral | Maintain a defensive approach by prioritizing high dividend sectors while taking advantage of volatility to accumulate select quality-growth names. |

| USD/PHP | Bullish | Buy US dollars on dips or near the 59.50–59.70 support levels. Ongoing US–Iran tensions show little sign of easing, which should continue to drive safe-haven demand and put pressure on the peso. Persistent inflation pressure will likely influence the future policy paths of both the BSP and the US Federal Reserve, providing additional support for the dollar. |

| G10 Currencies / US Dollar | Bearish | The prolonged conflict continues to favor the US Dollar over its G10 counterparts, though recovery may be sharp once risk sentiment improves. Major currencies EUR, GBP, and JPY are now at key levels and may see fresh lows if elevated energy prices are sustained. |

| Gold | Bullish | While initially reaching highs of USD 5,400 per troy ounce on safe-haven demand, gold has pared gains after higher oil prices sparked expectations of higher US inflation, delayed US Fed rate cuts, and a stronger US dollar. The precious metal has fallen just slightly below USD 5,000. Any further dip below USD 4,900 and we could see new entry opportunities at the USD 4,800 and USD 4,600 areas. Our long-term view is steady price appreciation as global central banks purchase gold to diversify reserves beyond the US dollar and US Treasuries. |

(Disclaimer: This is general investment information only and does not constitute an offer or guarantee, with all investment decisions made at your own risk. The bank takes no responsibility for any potential losses.)