Getting real, or nominal, with our GDP

Yes, it’s true. The country’s GDP considerably expanded by 12.8 percent during the first quarter of 2022, remarkably exceeding expectations.

Many people may not be aware of this substantial recovery. It’s not surprising because statistical agencies and news outlets reported 8.3 percent growth instead. But why is there a disparity? Which one should be considered?

The 12.8 percent figure is the nominal GDP growth rate of the country during the 1st quarter of 2022, while 8.3 percent is the real GDP growth rate. The difference between nominal and real GDP is that the former accounts for inflation while the latter does not.

This is where the GDP deflator comes in. For simplicity, the difference between nominal GDP and real GDP can be called the GDP deflator, and it is a measure of the effects of inflation relative to the base year. Hence, a GDP deflator would mean that today’s nominal GDP will “get deflated” by taking away the effects of inflation when GDP is expressed in the base year, or real GDP.

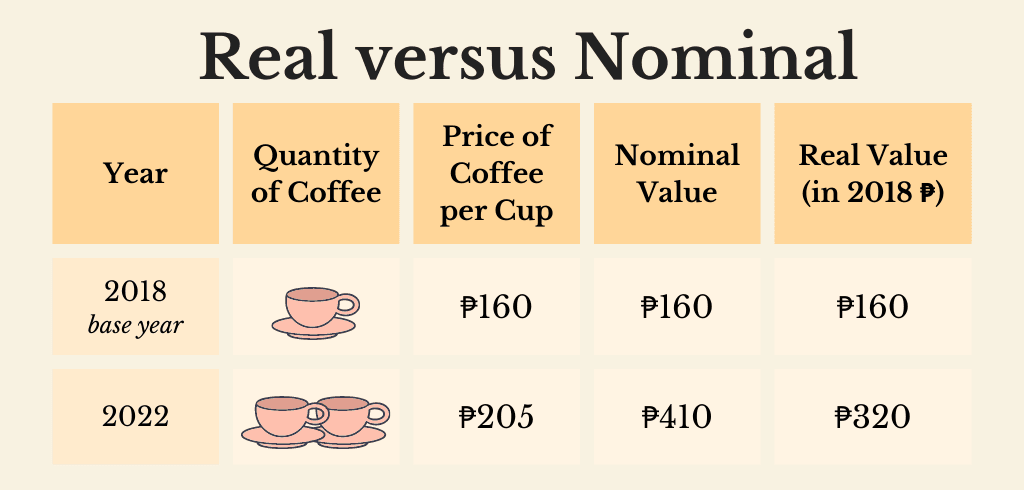

In the example above, the nominal value of PHP 410 “gets deflated” or shrinks to PHP 320 when expressed in real values indexed to the year 2018. That is, PHP 410 is the price now and PHP 320 is the corresponding value in 2018 prices.

When one wants to measure the rise in production over time without the influence of rising prices, then the measure of GDP should be at constant prices or prices from another year, usually called the base or index year. For the Philippines, 2018 is the base year for GDP.

This is the reason why news outlets or statistical agencies use real GDP to calculate GDP growth – they want to determine the expansion/contraction in the economy’s output without the effects of inflation.

But we do not live in the index or base year, i.e., we live in the “now”, at current prices. In the example, we are dealing with PHP 410 rather than PHP 320. This illustrates the importance of nominal values; investors are more concerned about current price levels rather than prices in 2018, and when people look at their salary, loans, expenses, etc., what they consider are current prices or values.

Nominal GDP is then crucial because it gives a snapshot of a country’s total output valued at the prices for which it was actually sold. In addition, nominal GDP is used for comparison purposes with other economic measures that are not adjusted for inflation.

An example of this is debt. Since debt is always in nominal terms, nominal GDP is the correct variable to employ to come up with a commonly observed metric called the debt-to-GDP ratio. In this case, the GDP denominator is even growing at a faster 12.8% nominal GDP growth clip than the 8.3% real GDP print, which should shrink the debt-to-GDP ratio faster.

Moving forward, a recovery in 2022 is still the call, with good nominal GDP prints expected. This is because there will likely be higher output because of more relaxed restrictions owing to the relatively low COVID-19 cases in the past months. There is also the continued infrastructure spending by the incoming government, especially its focus on growth rather than spending cuts, as highlighted by incoming Finance Chief Benjamin Diokno.

Yes, the real GDP print numbers might look smaller because of current high inflation. Nevertheless, it is still the nominal GDP numbers that will have bearing with regard to actual current growth and shrinking the debt-to-GDP ratio. And that is all good.

ANNA ISABELLE “BEA” LEJANO is a Research & Business Analytics Officer at Metrobank, in charge of the bank’s research on the macroeconomy and the banking industry. She obtained her Bachelor’s degree in Business Economics from the University of the Philippines School of Economics and is currently taking up her Master’s in Economics degree at the Ateneo de Manila University. She cannot function without coffee.