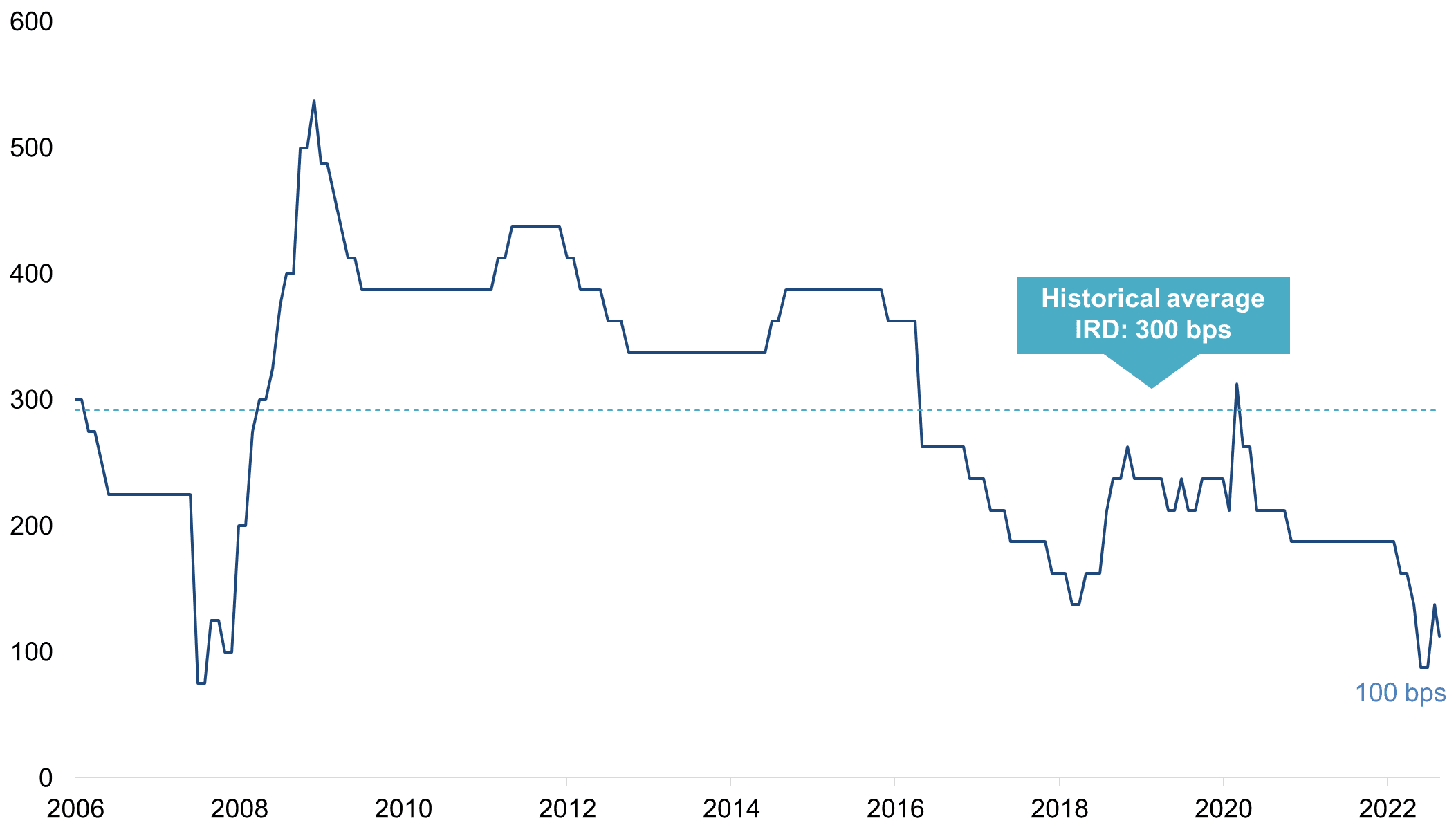

Historically, the spread between the BSP’s Reverse Repurchase (RRP) and the US Fed’s Federal Funds Rate (FFR) is around 3% or 300 bps. A narrow or tight IRD would mean that the home currency is under pressure as the foreign currency may have higher rates. This can happen when their own central bank is implementing strong monetary tightening measures, for instance. Conversely, a wide IRD would mean that the home currency is stable as it maintains an adequate differential with the foreign currency.

The USD/PHP exchange rate tells us the same story. With the US Fed busy with its own fight against inflation, the strong dollar has sent the foreign exchange market in heightened volatility this year. The peso has depreciated by 11% year-to-date (YTD). This compelled the BSP, similar to other central banks, to embark on its aggressive monetary tightening measures to keep up with the US’ key policy rate. The impact of a narrow IRD is not only on the exchange rate, but also on the inflationary effects that feed into the cost of goods. Hence, this is why Governor Medalla vowed to maintain the 100-bp IRD with the US key policy rate.