The reserve requirement refers to the minimum amount of bank deposits and deposit substitute liabilities (examples are demand, savings, time deposit and deposit substitutes) that banks must set aside as liquid cash that they cannot lend out. This is a requirement by central banks.

Reserve requirements are imposed on the peso liabilities of universal and commercial banks, thrift banks, rural banks and cooperative banks, and non-bank financial institutions with quasi-banking functions.

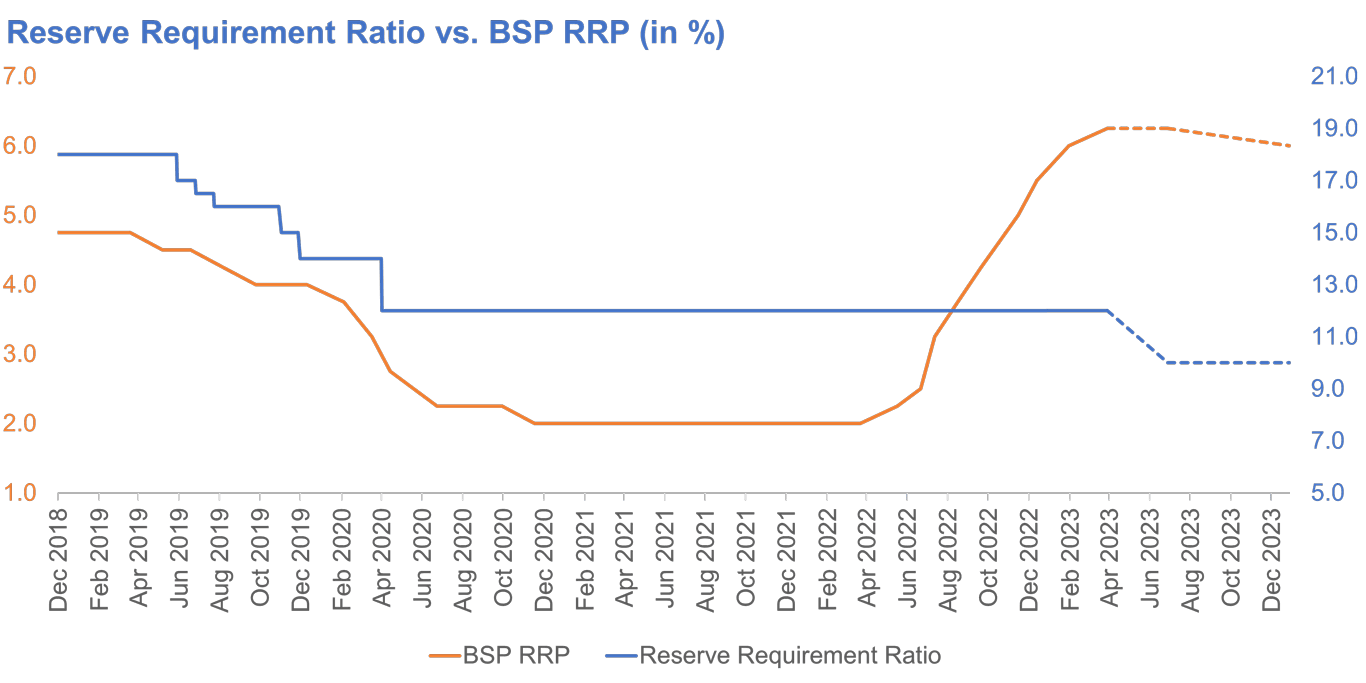

The reserve requirement ratio (RRR) for big banks is currently at 12%, which is said to be one of the highest in the region. Meanwhile, reserve requirements for thrift and rural lenders are at 3% and 2%, respectively.

The most basic formula for calculating the reserve requirement consists of multiplying the RRR by the total amount of deposits. For example, if Metrobank received PHP 100,000 in deposits and the reserve requirement ratio is set at 12%, the bank must maintain a minimum of PHP 12,000.