DOWNLOAD

DOWNLOAD

BVAL Yield Curve Outlook

By Gabriel Liboro

By Gabriel Liboro

Find out why the Bloomberg Valuation Service (BVAL) yield curve is steepening and how that may affect your investments more than you think.

FEATURED INSIGHTS

FEATURED INSIGHTSButter or BTr?

The Bureau of Treasury (BTr) just released their borrowing schedule for November and aside from the obvious similarities in their names, they took another line out of everyone’s favorite Korean Pop band BTS (sorry, Blackpink): Side steep, right-left, to my beat. Immediate reaction was for curve to steepen on the announcement, as they continued their weekly auction of Treasury bonds, opting to issue 5, 7 and 10Y bonds next month. You’re likely wondering how this affects you. How does the BTr’s borrowing program affect my investments? Why do the tenors matter? And for God’s sake why do I have this sudden urge to break into dance and dye my hair?

What is a yield curve?

As an investor, you’ve no doubt heard the terms “flat yield curve” or “steep yield curve” thrown around in the course of creating your investment portfolio. What does it all mean? To start with, a yield curve is just yields of each bond tenor plotted on a graph which shows where short-term and long-term yields are. In the Philippines, we look at the BVAL benchmark rates for a more accurate depiction of our curve. This curve tends to slope upward as investors prefer to be paid higher yields for longer-term securities which carry more risk. Rates move inversely to the price, so higher yields means cheaper bond prices and vice versa with lower rates equating to more expensive bonds. So what is the significance of the curve’s shape? A yield curve flattens when the difference between short-term and long-term rates decreases, while a steeper curve shows the difference between rates increase. A number of factors go into determining the movement of bond rates, like inflation, growth, interest rates, but for now the focus should be on supply. Got it? Let’s roll!

The Bureau of Treasury's November schedule moves yields higher

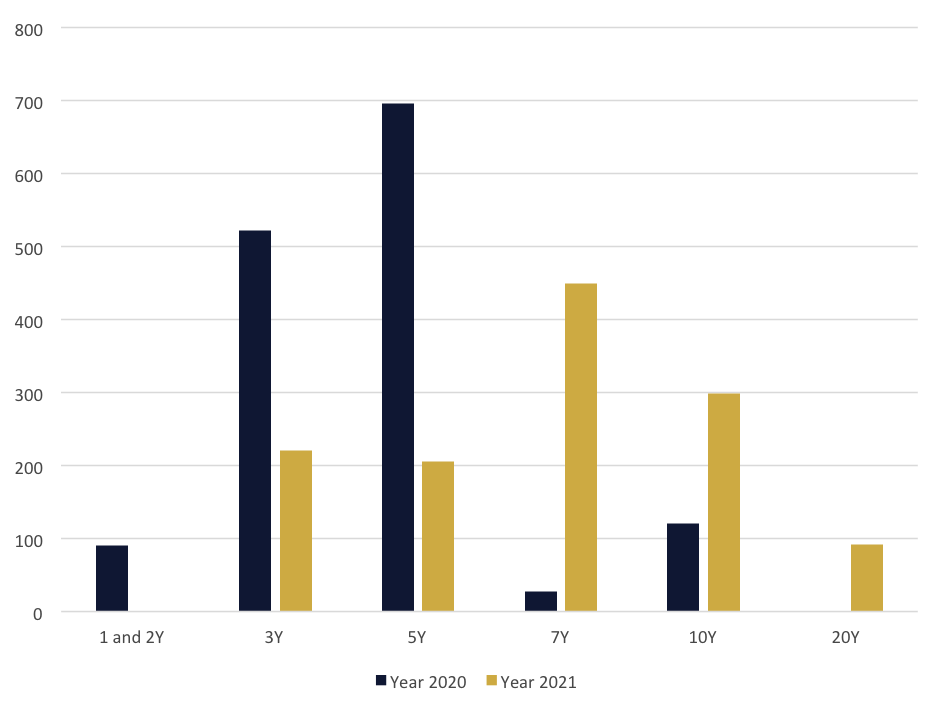

2020 vs 2021 Bond Tenor Issuances in Billions

Sliding back into the BTr’s announced schedule for November, they opted to issue tenors consistent with their preference in 2021, which is mostly middle to longer-dated bonds. This allows them to borrow money from investors for a longer duration at lower rates. Currently, the nation’s Overnight Borrowing Rate, a key tool of the BSP’s monetary policy, is at an historic low of 2.00% and doesn’t seem to be rising in the near-term. Aside from issuing bonds ranging from 5Y to 20Y this year, they’ve also stepped up the number of auctions per month since June, issuing bonds on a weekly basis instead of every other week like they did last year. It has caused a sharp adjustment in yields higher due to the supply risk I mentioned. The more supply there is in the market, the more pressure is applied for rates to move higher in those particular tenors. Even with blonde dyed hair, I may not look or dance like Jungkook so just let me show you because talk is cheap. In terms of the widening spread in BVAL rates at the start of 2021 and where we are today, the 3Y BVAL has risen from 2.088% to 2.8796%, which is about 80 basis points (bps) already. For color, the benchmark 5, 7 and 10Y rates are up 125 bps, 165 bps and 190bps, respectively.

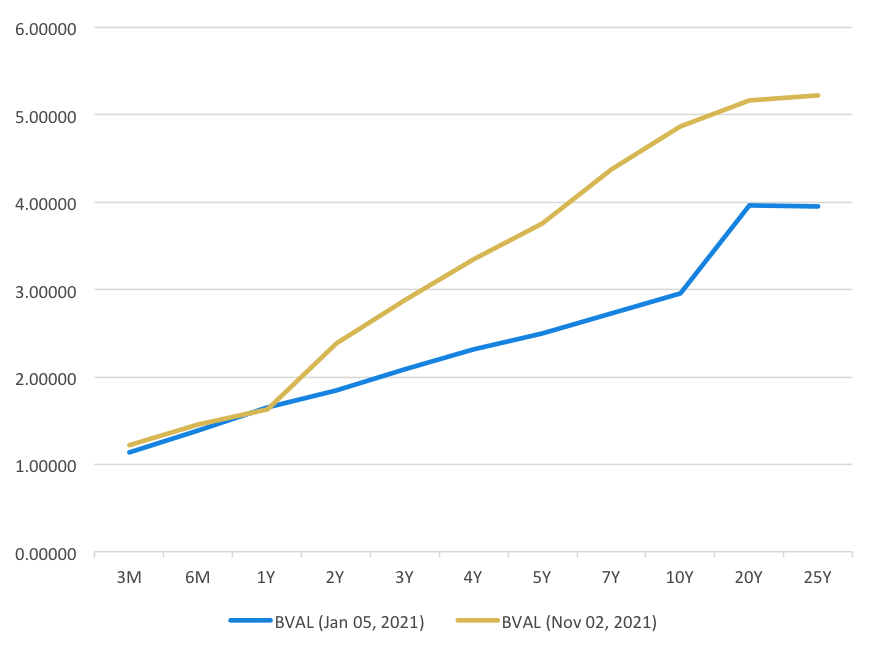

PHP BVAL Curve Start 2021 vs Current 2021

As shown in the charts, there’s been a steep ascent in bond yields mostly in the 7-10Y tenors due to BTr’s willingness to issue in this part of the curve compared to last year. The oversupply brought about by weekly auctions is causing institutional investors to avoid these securities and reposition their funds in bonds maturing within two years or Philippine T-bills. Unlike BTS merchandise that continues to see great demand even in a pandemic, Treasury bonds with increased supply are seeing less interest from the market, hence the sell-off and rise in yields.

Our Recommendations

Adding to the volatility in yields is our anticipation of the BSP eventually raising the overnight borrowing rate sometime in 2022 which would cause rates across the curve to all adjust higher. With that, it makes sense for your portfolio to be lighter on bonds for the meantime as we wait and see where yields end up this year. Like any good group of fans, we’re there for the highs and lows (literally in rates) and you know we don’t stop, but it’s advisable to stay nimble and invested in liquid shorter-term securities that you could shift to better yielding instruments once an opportunity presents itself. This year has been anything but smooth like butter (BTr?) but there’s still time to reassess your strategies heading into 2022 with an emphasis on further rising bond rates which should help you make better informed decisions. From experience, one of those should not be to dye your hair.