DOWNLOAD

DOWNLOAD

December 2023 Updates: Reassuring numbers call for revised forecasts

We have revised our outlook for a number of economic indicators based on the latest data.

By Metrobank Research

By Metrobank Research

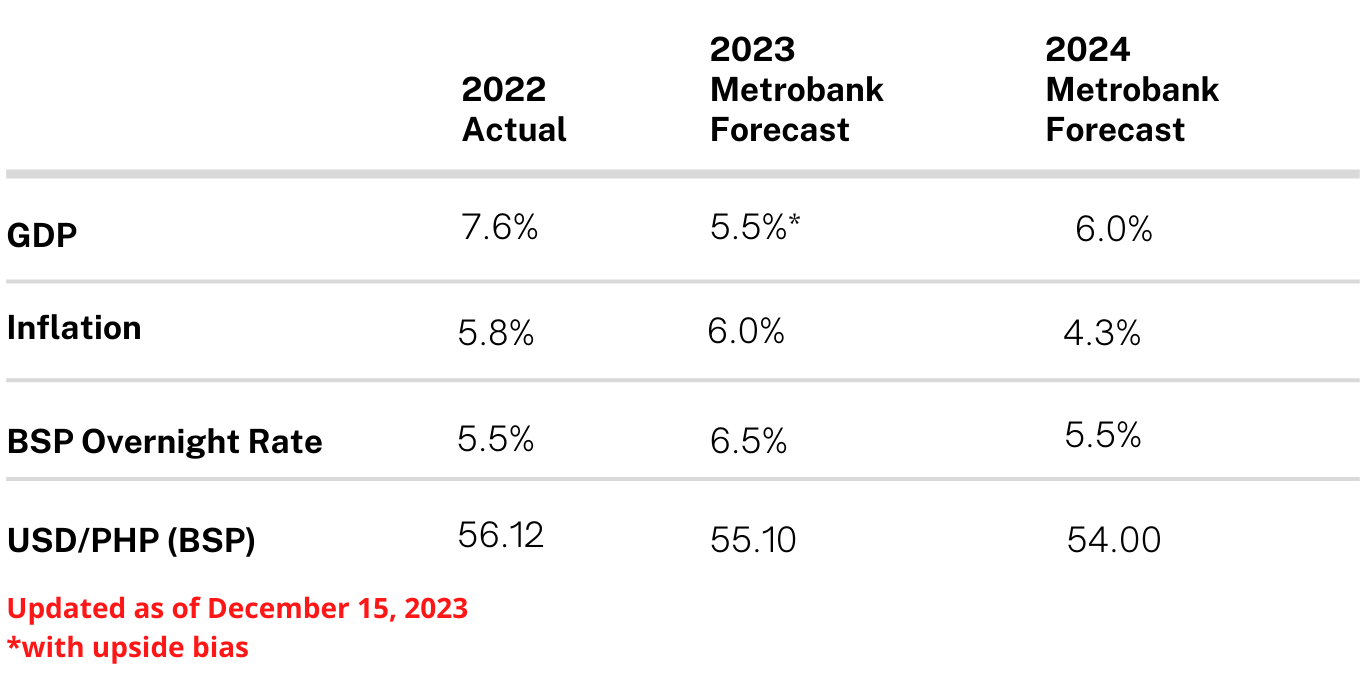

Philippines headline inflation eased further to 4.1% year-on-year in November from 4.9% in October (+0.16% month-on-month), driven by a slower annual increase in the prices of food and non-alcoholic beverages, transportation, as well as restaurants and accommodation services.

The lower-than-expected annual inflation rate is reassuring as it is slowly approaching the BSP’s target range of 2%-4% inflation. However, given the presence of existing geopolitical conflicts and lingering supply constraints, which could be exacerbated by the effects of El Niño until early next year, we see above-target inflation persisting through 2024.

Relative to the US Federal Reserve, we think that the BSP will take on a more gradual pace of rate cuts. Our base case is that the Fed will deliver its first cut in March, but the BSP will lag the pivot by two to three months to begin its easing cycle by June 2024.

Despite the recent move higher in the USD/PHP exchange rate, we expect remittances to build up during the holidays, which should provide relief for the peso and bring the exchange rate towards the year-end forecast of 55.10.

The dollar-peso exchange rate will likely trade in a tighter range of 53.00-56.00 next year, and we have revised our year-end 2024 forecast to 54.00 (from 54.40 previously) on the expectation of further dollar weakness as global markets aggressively price in Fed interest rate cuts.

Considering these developments, we have revised our forecasts for the following key macroeconomic indicators:

For more information on the performance and outlook for several macroeconomic indicators, as well as local macroeconomic news, please download the full report (released December 22, 2023) below.

December 2023 Updates: Reassuring numbers call for revised forecasts

The latest data suggest some changes in the trajectory of certain economic indicators.