Yields on gov’t debt rise despite dovish central banks

Yields on government securities (GS) rose last week even as global central banks kept benchmark rates steady.

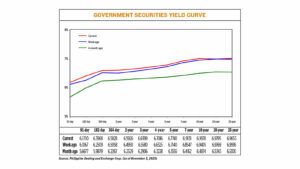

Bond yields, which move opposite to prices, went up by an average of 6.18 basis points (bps) week on week, based on PHP Bloomberg Valuation Service Reference Rates as of Nov. 3 published on the Philippine Dealing System’s website.

Yields on the 91-, 182-, and 364-day Treasury bills (T-bills) rose by 6.43 bps (to 6.171%), 14.59 bps (6.3968%), and 7.7 bps (3.5828%), respectively.

At the belly of the curve, rates of the two-, three-, four-, five-, and seven-year Treasury bonds (T-bonds) increased by 9.76 bps (to 6.5926%), 8.19 bps (6.6399%), 6.91 bps (6.7016%), 6 bps (6.774%), and 5.84 bps (6.9131%), respectively.

At the long end, the 10- and 20-year papers increased by 5.73 bps (to 6.9978%) and 0.26 bp (6.9795%), respectively.

Only the 25-year T-bond declined, with its yield dropping by 3.42 bps to 6.9653%.

Total GS volume traded on Friday climbed to PHP 16.428 billion from PHP 13.694 billion on Oct. 27.

A bond trader said the GS market was generally quiet last week due to the shortened trading week. Financial markets were closed on Oct. 30, Nov. 1 and 2 for public holidays.

On Friday, some bargain hunting occurred for papers with long tenors as yields tracked the overnight movement in US Treasuries, the trader said.

Another bond trader attributed last week’s yield movements to the lower US Treasury rates as the European Central Bank (ECB), US Federal Reserve, and Bank of England (BoE) kept borrowing costs steady in their respective meetings.

“The pause in tightening should relieve the BSP (Bangko Sentral ng Pilipinas) of some pressure to tighten further after its out-of-cycle hike,” the second trader said.

“However, the focus will still be on the inflation print for October and the BSP has put itself in a situation where it can tighten further if necessary,” the trader added.

The Fed last week kept its target rate steady at the 5.25%-5.5% range for a second straight meeting and hinted at a possible end to its tightening campaign.

Meanwhile, the ECB and BoE had also maintained interest rates. ECB has kept its key rate at 4% after 10 straight rate hikes, while BoE paused twice in a row at 5.25% after its 14 back-to-back increases.

For its part, the BSP hiked its policy rate by 25 bps to a 16-year high of 6.5% in an off-cycle move on Oct. 26.

BSP Governor Eli M. Remolona, Jr. said another increase could be on the table at the Monetary Board’s Nov. 16 meeting, depending on upcoming data releases.

For this week, investors will stay cautious before the release of October inflation data on Tuesday, both traders said.

A BusinessWorld poll last week yielded a median estimate of 5.7% for October headline inflation. If realized, this would be slower than the 6.1% in September and the 7.7% in October last year.

“If headline inflation surprises on the upside, bargain hunting will pull back and yields will definitely rise,” the first bond trader said. — A.C. Abestano

This article originally appeared on bworldonline.com