Yields on government debt go up to track global rates

Yields on local government securities (GS) traded at the secondary market climbed last week to track the rise in US Treasury rates due to the conflict in the Middle East and bets on the US Federal Reserve’s next move.

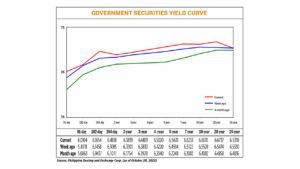

GS yields, which move opposite to prices, went up by an average of 8.25 basis points (bps) week on week, based on PHP Bloomberg Valuation Service Reference Rates as of Oct. 20 published on the Philippine Dealing System’s website.

Rates increased almost across the board, except for 25-year Treasury bonds (T-bonds), which slipped by 0.12 bp to fetch 6.5318%.

Yields at the short end of the curve went up, with the 91-, 182- and 364-day Treasury bills rising by 13.93 bps, 1.96 bps and 15.33 bps, respectively, to 6.0104%, 6.1654% and 6.4618%.

At the belly of the curve, yields on the two-, three-, four-, five-, and seven-year T-bonds likewise rose by 5.38 bps (to 6.3839%), 5.79 bps (6.4409%), 8 bps (6.502%), 10,37% (6.5631%) and 11.11 bps (6.6233%), respectively.

At the long end, the 10- and 20-year debt papers saw their yield go up by 6.42 bps (6.617%) and 12.63 bps (6.6737%), respectively.

Total GS volume traded last week surged to PHP 13.53 billion from PHP 3.99 billion a week earlier.

Last week’s yield movements were driven by the rising US Treasury yields amid hawkish Fed remarks, analysts said.

“This affected sentiment for local GS, which also followed the same trend with other countries albeit to a lesser degree. Bangko Sentral ng Pilipinas (BSP) may need to follow the action of the Fed as inflation locally is also still elevated and the geopolitical conflict in the Middle East is pressuring oil prices to move higher,” Security Bank Corp. Chief Investment Officer for Trust and Asset Management Group Noel S. Reyes said in an e-mail.

On Thursday, the 10-year US Treasury yield briefly crossed 5% following hawkish remarks by Federal Reserve Chair Jerome H. Powell, while the Middle East conflict kept investors jittery, Reuters reported.

Speaking at the Economic Club of New York on Thursday, Mr. Powell said the US economy’s strength and continued tight labor markets could require tougher borrowing conditions to control inflation.

Atlanta Fed President Raphael Bostic told CNBC that while inflation remained too high, it is falling amid mounting evidence of an economic slowdown, and that could open the door to a softer monetary policy late next year.

BofA Global Research said it now expects the US central bank to deliver a 25-basis-point rate hike in December instead of November.

Traders see a near 99% chance the Fed will keep benchmark rates unchanged in November, while their bets for a pause in December stood at around 79%, according to CME’s FedWatch Tool.

Meanwhile, Philippine headline inflation stood at 6.1% in September, up from 5.3% in August.

This brought the nine-month average to 6.6%, higher than the Bangko Sentral ng Pilipinas’ (BSP) 5.8% forecast and 2-4% target for the year

The Monetary Board has kept the policy rate at a near 16-year high of 6.25% at its last four meetings. It raised borrowing costs by 425 bps from May 2022 to March 2023 to help bring down inflation.

BSP Governor Eli M. Remolona, Jr. earlier said the Monetary Board could consider hiking borrowing costs by 25 bps in their Nov. 16 review amid rising inflation.

“Local bond yields took their cue from global bond yields, which were on the uptick due to the outlook for global inflation,” ING Bank N.V. Manila Senior Economist Nicholas Antonio T. Mapa said in an e-mail.

Jonathan L. Ravelas, senior adviser at Reyes Tacandong & Co., likewise said in a Viber message that the yield movements were influenced by the movement in 10-year US Treasury yields.

“It hit its highest levels since 2007 close to 5%, domestic yield followed suit still driven by the hawkish pause and higher rates for longer,” Mr. Ravelas said.

For this week, he said yields could move sideways or higher as the market awaits the release of October inflation data.

For his part, Mr. Reyes said that GS yield movements will depend on US economic data releases.

“This will dictate price action but granted that it is an end of month week, some bottom-fishing may arise, cushioning any further bouts of further higher yield swings. We are near the peak of terminal policy rates also by the BSP and could entice such movement,” he said.

“This week should be more of the same, with geopolitical developments taking center stage,” Mr. Mapa added. — Lourdes O. Pilar with Reuters

This article originally appeared on bworldonline.com