Yields on government debt go down

YIELDS on government securities (GS) continued to decline last week due to a lack of catalysts as the end of the year nears.

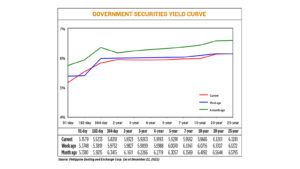

GS yields at the secondary market fell by an average of 6.21 basis points (bps) week on week, based on the PHP Bloomberg Valuation (BVAL) Service Reference Rates as of Dec. 22 published on the Philippine Dealing System’s website.

Most tenors saw their yields decline last week, with rates of the 91- and 364-day Treasury bills (T-bill) dropping by 21.69 bps and 15.14 bps to 5.1579% and 5.8218%, respectively. On the other hand, the 182-day T-bill went up by 13.42 bps to yield 5.5233%.

Rates of tenors at the belly likewise dropped. Yields on the two-, three-, four-, five-, and seven-year Treasury bonds (T-bonds) went down by 5.04 bps (5.9323%), 6.96 bps (5.9203%), 7.95 bps (5.9193%), 7.79 bps (5.9291%), and 5.69 bps (5.9592%), respectively.

Yields at the long end were mixed. The 10- and 20-year papers saw their rates decline by 10.51 bps and 1.06 bps to 5.9665% and 6.1201%, respectively, while the 25-year paper inched up by 0.09 bp to yield 6.1281%.

Total GS volume traded reached P22.51 billion on Friday, more than three times the P7.46 billion recorded on Dec. 15.

The continued drop in GS yields last week was due to a lack of catalysts and bond supply, a bond trader said in a Viber message.

“Bond yields dropped as investors scramble to find investment outlets. The move was also supported by a drop in global yields,” the bond trader said.

The lack of catalysts was likely due to risk aversion and the “higher for longer” policy stance of local monetary authorities, Oikonomia Advisory & Research, Inc. President and Chief Economist John Paolo R. Rivera said in a separate Viber message.

However, increased consumption and various economic activities brought by the holiday season can help drive trading in the last week of the year, he said.

“Trading is usually active in the latter parts of the year in anticipation of slower flow of funds as the new year starts. Increased consumption due to holidays is also indicative of an active economy,” Mr. Rivera added.

“Total borrowing remains to be constrained as interest rates will remain elevated given the hawkish stance of BSP (Bangko Sentral ng Pilipinas),” he added.

The BSP is unlikely to start policy easing in the next few months and will only consider cutting rates if inflation settles at the midpoint of the 2-4% target, its chief said last week.

“We’re unlikely to cut rates in the next few months. We’re in a higher for longer (scenario). When I say hawkish, that basically means high for a while,” BSP Governor Eli M. Remolona, Jr. told reporters.

The Monetary Board this month kept its benchmark rate at a 16-year high of 6.5% for a second straight meeting. Interest rates on the overnight deposit and lending facilities were also left unchanged at 6% and 7%, respectively.

From May 2022 to October this year, the BSP raised borrowing costs by a cumulative 450 bps to tame inflation.

The BTr plans to borrow a total of P435 billion during the first quarter, with the bulk coming from T-bond auctions, based on its borrowing plan released last week.

For the week, Mr. Rivera said trading may pick up as traders may take advantage of the momentum seen in the past weeks.

“As expectations level off and as traders harness the holiday effects, trading may increase albeit at a slower rate. The last [three] days are crucial as it can make or break annual targets,” he said.

“Bond trading will remain to be constrained given a foreseeable elevated policy rates. Higher cost of borrowing inhibits bond issuance,” Mr. Rivera added.

GS yields may move sideways with an upward bias, with investors expected to cash in on their gains, the bond trader said.

“For next year, it will be bumpy as the market’s pricing in of rate cuts and the corresponding reaction in bonds assume that yield curve inversion will remain. This may not be consistent with expectations on inflation,” the trader added. — Bernadette Therese M. Gadon

This article originally appeared on bworldonline.com