Gov’t debt yields go up on inflation concerns

Yields on government securities (GS) traded at the secondary market went up across the board last week amid inflation concerns here and abroad.

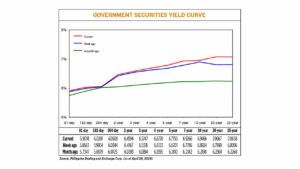

GS yields, which move opposite to prices, went up by 9.77 basis points (bps) on average week on week, data from the PHP Bloomberg Valuation Service Reference Rates as of April 26 published on the Philippine Dealing System’s website showed.

Rates across all tenors went up last week. At the short end of the curve, the 91-, 182-, and 364-day Treasury bills climbed by 3.55 bps (to 5.9018%), 3.97 bps (6.0201%), and 1.64 bps (6.0508%), respectively.

At the belly, yields on the two-, three-, four-, five-, and seven-year Treasury bonds (T-bonds) rose by 4.27 bps (to 6.4594%), 3.71 bps (6.5747%), 6.37 bps (6.677%), 10.49 bps (6.775%), and 14.80 bps (6.9266%), respectively.

Lastly, at the long end of the curve, the rate of the 10-year debt paper rose by 5.42 bps to 6.9466% and the 20- and 25-year T-bonds surged by 26.77 bps (to 7.0667%) and 26.52 bps (7.0658%), respectively.

However, GS volume traded slipped to P11 billion last week from P14.66 billion on April 19.

Yields on government debt rose due to inflation concerns at home and abroad due to the impact of geopolitical tensions in the Middle East on oil prices, analysts said.

“Market participants [last week] considered the potential inflationary impact from higher energy prices due to the recent domestic shortages and peso depreciation,” a bond trader said in an e-mail.

In the past few weeks, Luzon and Visayas were placed under red and yellow alert status amid insufficient power supply to meet demand.

“Upside inflation risks both here and abroad [are] keeping higher rates for longer and are pushing rates closer to 2023 levels,” Jonathan L. Ravelas, managing director of eManagement for Business and Marketing Services, said in a Viber message.

“Rising oil prices would raise fears by investors that there will be some inflation down the road,” Peter Lee U, dean of the University of Asia and the Pacific’s School of Economics, said in an e-mail.

On Friday, Brent crude futures settled up 49 cents or 0.55% to $89.50 a barrel, Reuters reported. US West Texas Intermediate crude futures settled up 28 cents or 0.34% to $83.85 a barrel.

Iran has said that it had no plans to retaliate following an apparent Israeli drone attack within its borders, which in turn followed an Iranian missile and drone attack on Israel days before.

“The effect of the geopolitical tensions in the Middle East have been more prominent in our local currency given the peso’s depreciation against the dollar,” Alessandra P. Araullo, chief investment officer at ATRAM Trust Corp., said in a Viber message.

On Friday, the peso closed at P57.71 per dollar, rising by seven centavos from the day prior. However, week on week, the local unit weakened by six centavos from its P57.65 finish on April 19.

“Trading for [last] week remained light and as local yields were still highly sensitive to US Treasury yields’ movement. The lack of local catalysts coupled with the hawkish tone of the BSP (Bangko Sentral ng Pilipinas) and the Fed (US Federal Reserve) all contributed to a shallow risk appetite for the week,” Ms. Araullo added.

“Markets may have already priced in that the BSP may keep rates unchanged for the first half of the year given the expected upward trend in inflation for the second quarter 2024. This was reflected when yields surged by 20-50 bps across on the second week of April alone. Market participants have since remained defensive as overall sentiment has soured,” she said.

BSP Governor Eli M. Remolona, Jr. this month said they could begin their easing cycle in early 2025 if price risks persist, but they could still cut rates by 25 bps in the third quarter if inflation is within target and economic growth is weak.

The Monetary Board kept its target reverse repurchase rate unchanged at a near 17-year high of 6.5% this month. It hiked borrowing costs by 450 bps from May 2022 to October 2023 to help bring down elevated inflation.

Meanwhile, a hotter-than-expected consumer price inflation report for March pushed back expectations of when the Fed will begin cutting interest rates, with markets pricing in a 70% chance of the first cut coming in September, CME FedWatch Tool showed, Reuters reported.

Traders are pricing in 43 bps of easing in 2024, drastically less than the 150 bps they anticipated at the start of this year.

The shifting expectations of US rates have lifted Treasury yields and the dollar, casting a shadow on the currency market.

For this week, Ms. Araullo expects GS yield movements to be driven by the results of the T-bond auction on Tuesday as well as the Fed’s policy meeting on April 30-May 1.

“Investors hope to get better guidance on future monetary plans and the Fed’s update on their progress in their goal to bring inflation down. In addition, markets will also be looking at the latest nonfarm payrolls as a stronger figure may solidify the view that the Fed will have to keep rates higher for longer. These will be the key factors that will influence the bond market in the coming weeks,” she said.

“For the coming month, the local factors that will continue to shape the bond market will be the local CPI (consumer price index) result and the BSP monetary policy meeting on May 16. Investors will look for further concrete guidance from BSP Governor Remolona on his view on inflation and monetary policy. The local market will also be influenced by the movement of US yields as future macroeconomic data in the US may continue to indicate that rates may stay higher. Market will also keep track of the speeches of Fed officials for more guidance,” Ms. Araullo added.

April Philippine inflation data will be released on May 7. — A.C. Abestano with Reuters

This article originally appeared on bworldonline.com