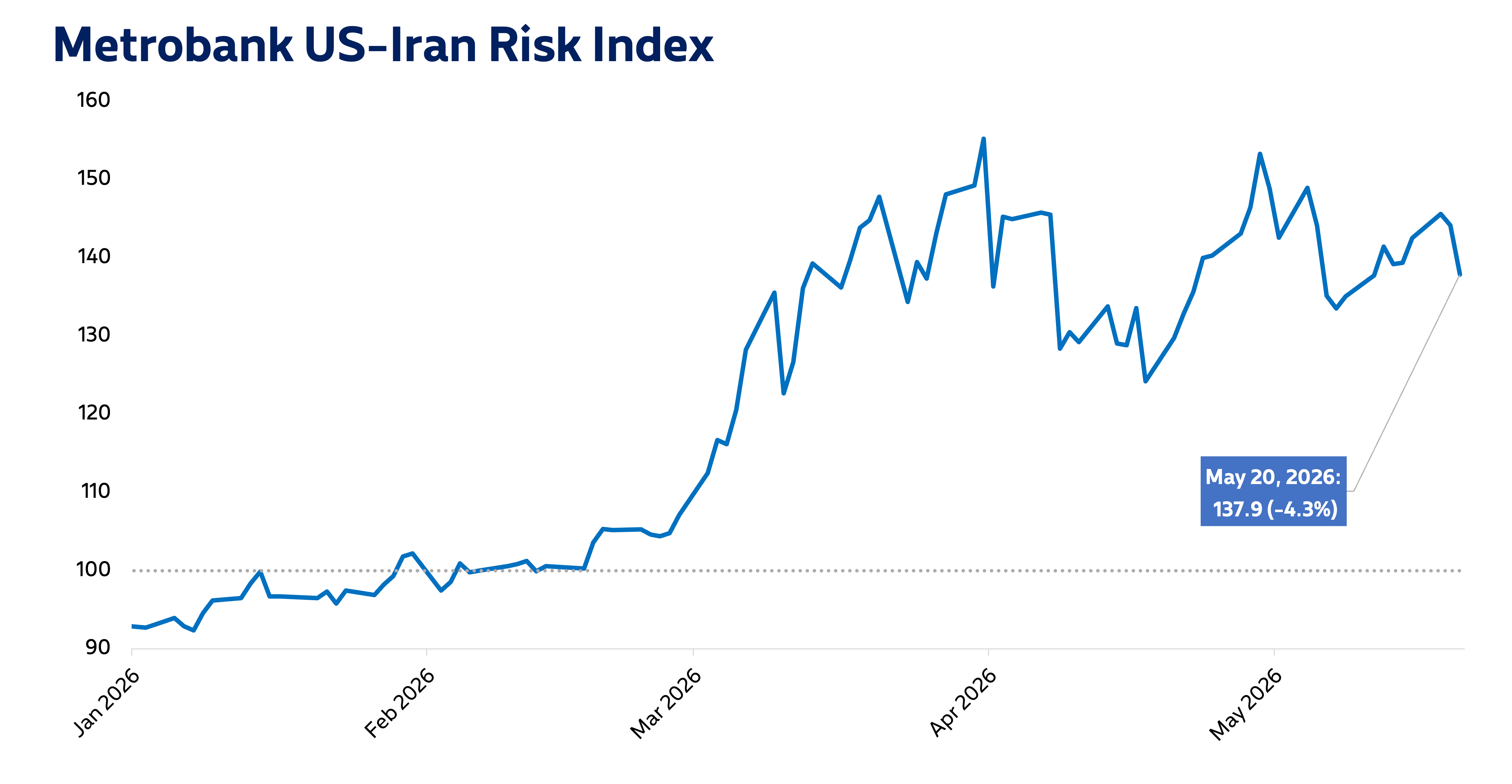

Metrobank’s US-Iran Risk Index settled at 137.9 on May 20th, 4.3% lower than its value of 144.1 on the prior trading day.

Global oil prices fell on Wednesday following comments from US President Donald Trump that US-Iran talks were in their “final stages,” according to Reuters. Still, the Strait of Hormuz’s closure has kept the commodity’s price elevated. Brent Crude closed at USD 105 per barrel on Wednesday, compared to its closing price of USD 111 on Tuesday, UK trading, according to data compiled by Bloomberg.

Though Trump has threatened further attacks on Iran should a deal fail to materialize, he also said that the US is willing to wait a few days for “the right answers” in ongoing talks, according to Reuters. While the ceasefire has led to slightly tempered risk levels in financial markets, upside risks remain amid possibility of military escalation.

Meanwhile, the benchmark 10-year US Treasury yield pulled back on Wednesday, US trading, on lower oil prices. This comes after a spike in yields across the US Treasury curve earlier this week due to a worsening inflation outlook, with the 30-year US Treasury yield hitting its highest levels since the global financial crisis on Tuesday, US time, according to CNBC.

Additionally, the US dollar index softened on Wednesday, US trading, due to lower oil costs and ongoing US-Iran negotiations. The peso remained weak, however, leading to the dollar-peso exchange rate closing little changed at 61.74 on Wednesday, Philippine time.

Metrobank still sees elevated risk and volatility in the near-term while a peace deal has not been struck. Oil prices are poised to stay high, as global supply remains constricted due to the war’s impact on Middle East oil facilities. Consequently, domestic inflation is expected to quicken in the coming months, which will put upward pressure on Philippine bond yields.

Moreover, Metrobank forecasts continued rate hikes by the Bangko Sentral ng Pilipinas (BSP) this year to stem accelerating inflation. Finally, Metrobank expects the dollar-peso exchange rate to stay elevated, as dollar demand weighs on a weak peso.