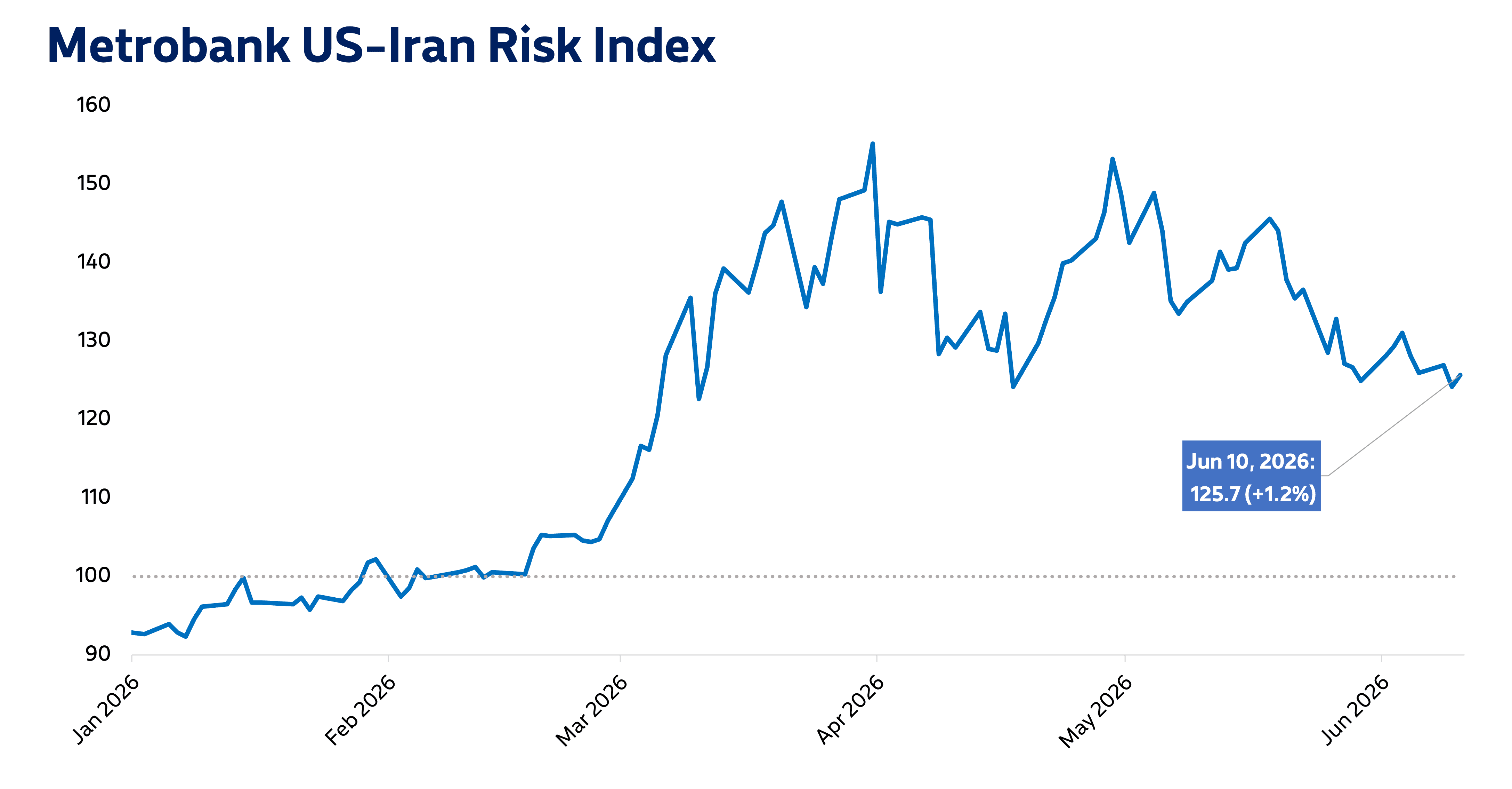

Metrobank’s US-Iran Risk Index settled at 125.7 on June 10, up by 1.2% from 124.2 the prior trading day.

Global oil prices rose, following threats from US President Donald Trump of a “very hard” attack on Iran if a peace deal is not reached, according to Reuters. Brent crude futures settled higher on Wednesday, UK trading, according to data compiled by Bloomberg.

The US launched multiple fresh strikes on Iran soon afterward, pushing oil prices further up in early Thursday trade. Risks remain tilted to the upside, with the ceasefire continually being breached and a deal feeling further from reach.

The US dollar index saw slight gains on Wednesday from renewed safe-haven flows. Meanwhile, the benchmark US 10-year Treasury yield rose by nearly 4 basis points (bps) after US CPI inflation was reported to have reached a 3-year high in May due to higher energy prices.

Metrobank sees elevated risk and volatility in the near-term, as the US and Iran continue attacks. Oil prices are poised to stay high, as global supply remains constricted due to the war’s impact on Middle East oil facilities. Domestic inflation is expected to exceed the Bangko Sentral ng Pilipinas (BSP)’s target this year, which will put upward pressure on Philippine bond yields.

Moreover, Metrobank forecasts continued rate hikes by the BSP this year to stem accelerating inflation. Finally, Metrobank expects the dollar-peso exchange rate to stay elevated, as dollar demand weighs on a weak peso.