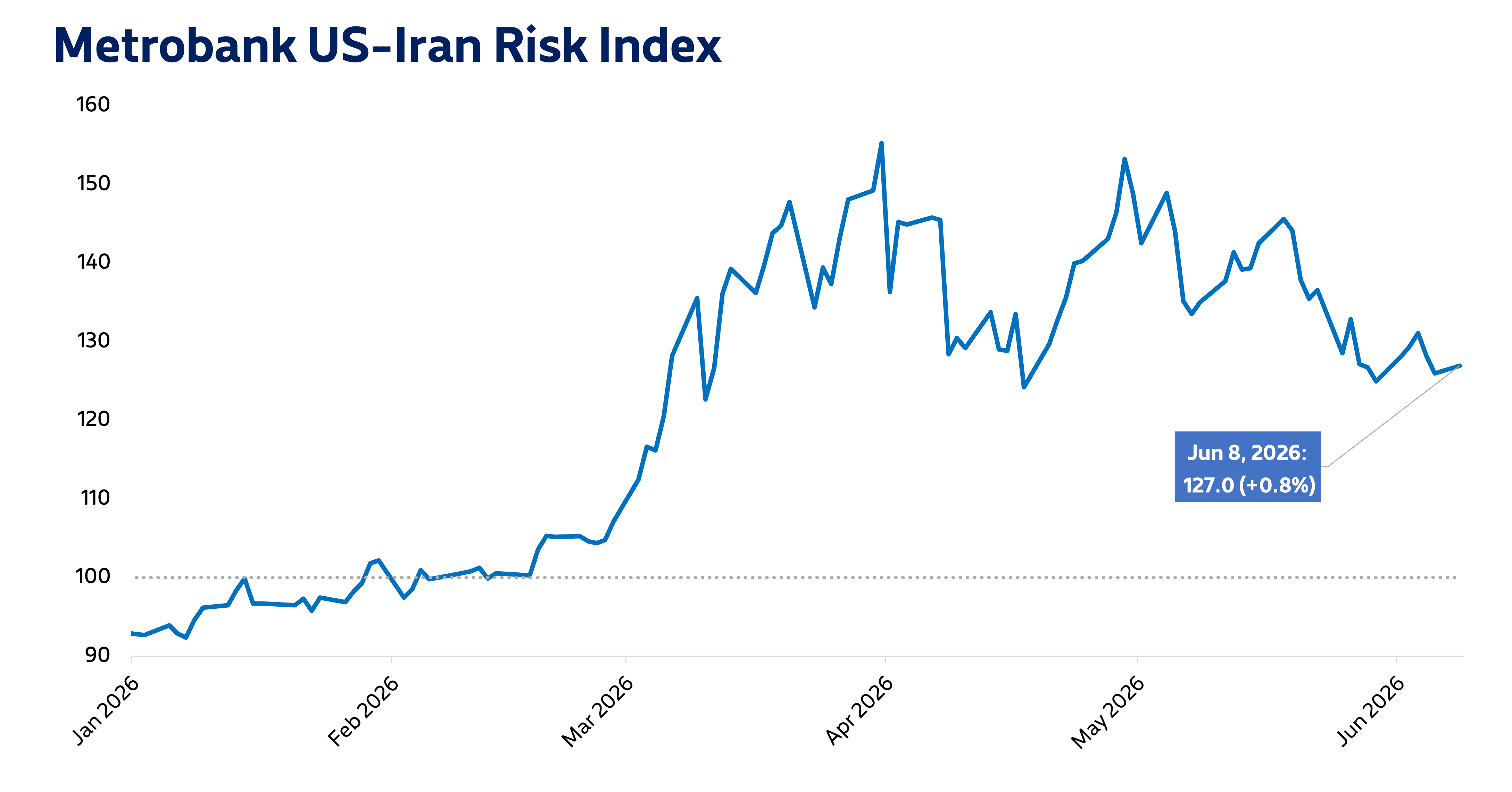

Metrobank’s US-Iran Risk Index settled at 127.0 on June 8, up by 0.8% from 126.0 the prior trading day.

Global oil prices rose as much as 5% during early UK trade on Monday, as Israel and Iran exchanged military strikes, according to Reuters. The commodity eventually pared most of these gains later in the day, as the two countries agreed to halt attacks. Brent crude futures still settled higher compared to the previous trading day at USD 94.25 per barrel, according to data compiled by Bloomberg.

Meanwhile, the benchmark 10-year US Treasury yield climbed by 3 basis points, as market players reacted to Israel-Iran hostilities and a more hawkish outlook for the US Federal Reserve. Meanwhile, the US dollar index was steady on Monday, with the dollar-peso exchange rate closing at 61.69 during Philippine trading.

While market players appear to price lower levels of risk compared to the onset of the war, the lack of a concrete peace deal and continued military attacks keep risks elevated.

Metrobank sees elevated risk and volatility in the near-term, given the lack of progress in US-Iran negotiations. Oil prices are poised to stay high, as global supply remains constricted due to the war’s impact on Middle East oil facilities. Domestic inflation is expected to exceed the Bangko Sentral ng Pilipinas (BSP)’s target this year, which will put upward pressure on Philippine bond yields.

Moreover, Metrobank forecasts continued rate hikes by the BSP this year to stem accelerating inflation. Finally, Metrobank expects the dollar-peso exchange rate to stay elevated, as dollar demand weighs on a weak peso.