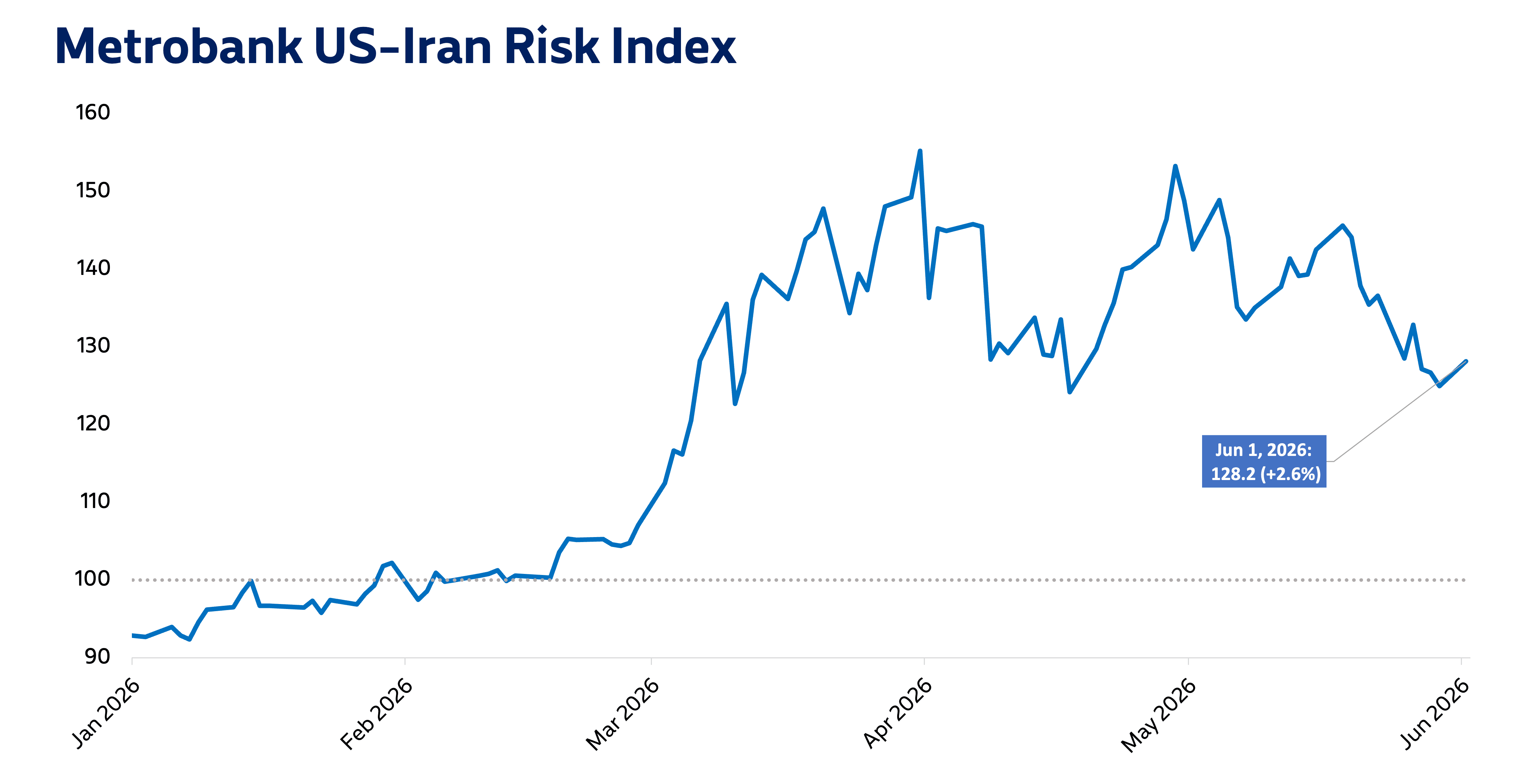

Metrobank’s US-Iran Risk Index settled at 128.2 on June 1st, 2.6% higher than its value of 125.0 on the prior trading day.

Global oil prices moved higher on news that Iran halted negotiations with the US, despite US President Donald Trump claiming that talks were progressing at a “rapid pace,” according to Reuters.

On top of stalled talks, Reuters also reported that Iran is planning to completely block the Strait of Hormuz. Market players reacted to the contradicting headlines by pricing in heightened risks, with Brent Crude closing at nearly USD 95 per barrel on Monday, UK trading, according to data compiled by Bloomberg.

The benchmark 10-year US Treasury yield also edged slightly higher during US trading. Meanwhile, the US dollar strengthened, as increased uncertainties pushed investors toward the safe haven asset. The dollar-peso exchange rate closed higher at 61.75 on Monday, Philippine trading.

Metrobank sees elevated risk and volatility in the near-term, as US-Iran negotiations remain fragile. Oil prices are poised to stay high, as global supply remains constricted due to the war’s impact on Middle East oil facilities. Consequently, domestic inflation is expected to quicken in the coming months, which may put upward pressure on Philippine bond yields.

Moreover, Metrobank forecasts continued rate hikes by the Bangko Sentral ng Pilipinas (BSP) this year to stem accelerating inflation. Finally, Metrobank expects the dollar-peso exchange rate to stay elevated, as dollar demand weighs on a weak peso.