Economy3 MIN READ

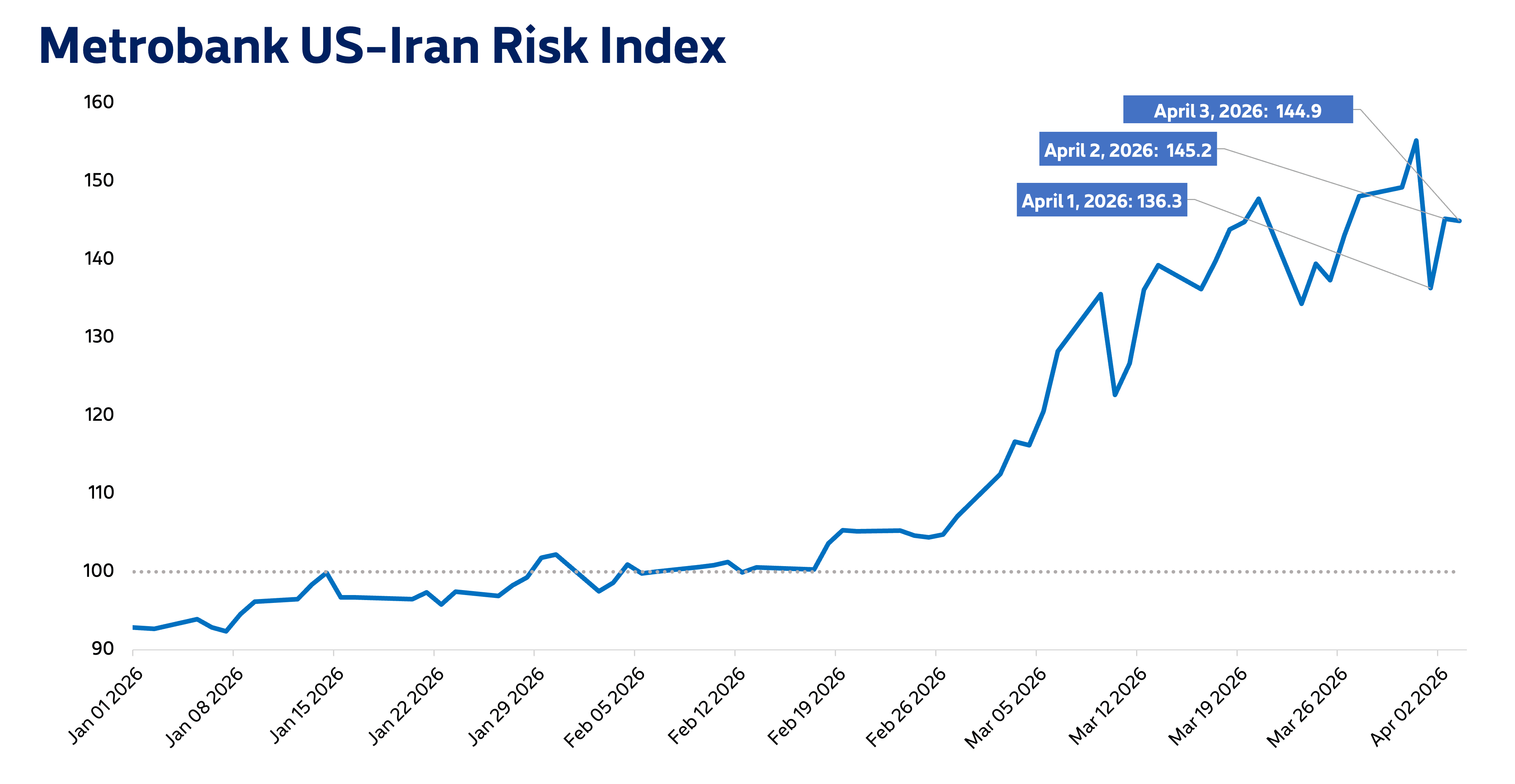

Metrobank US-Iran Risk Index: Dire straits

The struggle to reopen the Strait of Hormuz continues.

April 6, 2026 by Metrobank, Investment Counselor Department

Share this article:

Metrobank’s US-Iran Risk Index settled at 144.9 at the end of last week, April 3. Take note that US equity and commodity markets were closed on that day, while the US bond market had a half-day trading day in observance of the Good Friday holiday.

Global oil prices had settled slightly lower in the latter half of last week following its spike on Tuesday. While market players were somewhat calmed by US President Donald Trump’s claim that the war would end soon, the lack of clarity on the reopening of the Strait of Hormuz, a critical transit point for global oil shipments, kept oil prices elevated. Brent crude closed at USD 109 per barrel during its last trading day on April 2, according to data compiled by Bloomberg.

Moreover, the US dollar continued to strengthen, as uncertainties fueled safe-haven demand for the greenback. Meanwhile, inflation concerns pushed US Treasury yields upwards during the US bond market’s half-day trading session on April 3.

Over the weekend, Trump threatened to unleash devastating attacks on Iran if the Strait of Hormuz stayed closed by Tuesday, according to Al Jazeera. Iran responded by threatening further retaliatory attacks, according to the BBC. Even with Trump affirming a swift resolution to the conflict, these sharp escalations will likely keep market players on the edge, as chances for the strait’s reopening continue to dim.

Metrobank still expects upside oil pressure, as global oil supply remains constricted. We also expect the Bangko Sentral ng Pilipinas to raise their policy interest rate this year to combat rising inflation. Lastly, we see the dollar-peso remaining elevated in the near-future, as the dollar continues to strengthen on safe-haven demand.

Metrobank’s US-Iran Risk Index measures the amount of risk that the ongoing conflict presents to financial markets. It considers the general risk sentiment of investors and inflationary pressure brought by the conflict. A value of 100 denotes a normal level of risk based on market levels prior to the conflict’s escalation, while values greater than 100 imply increasing levels of risk.