Economy2 MIN READ

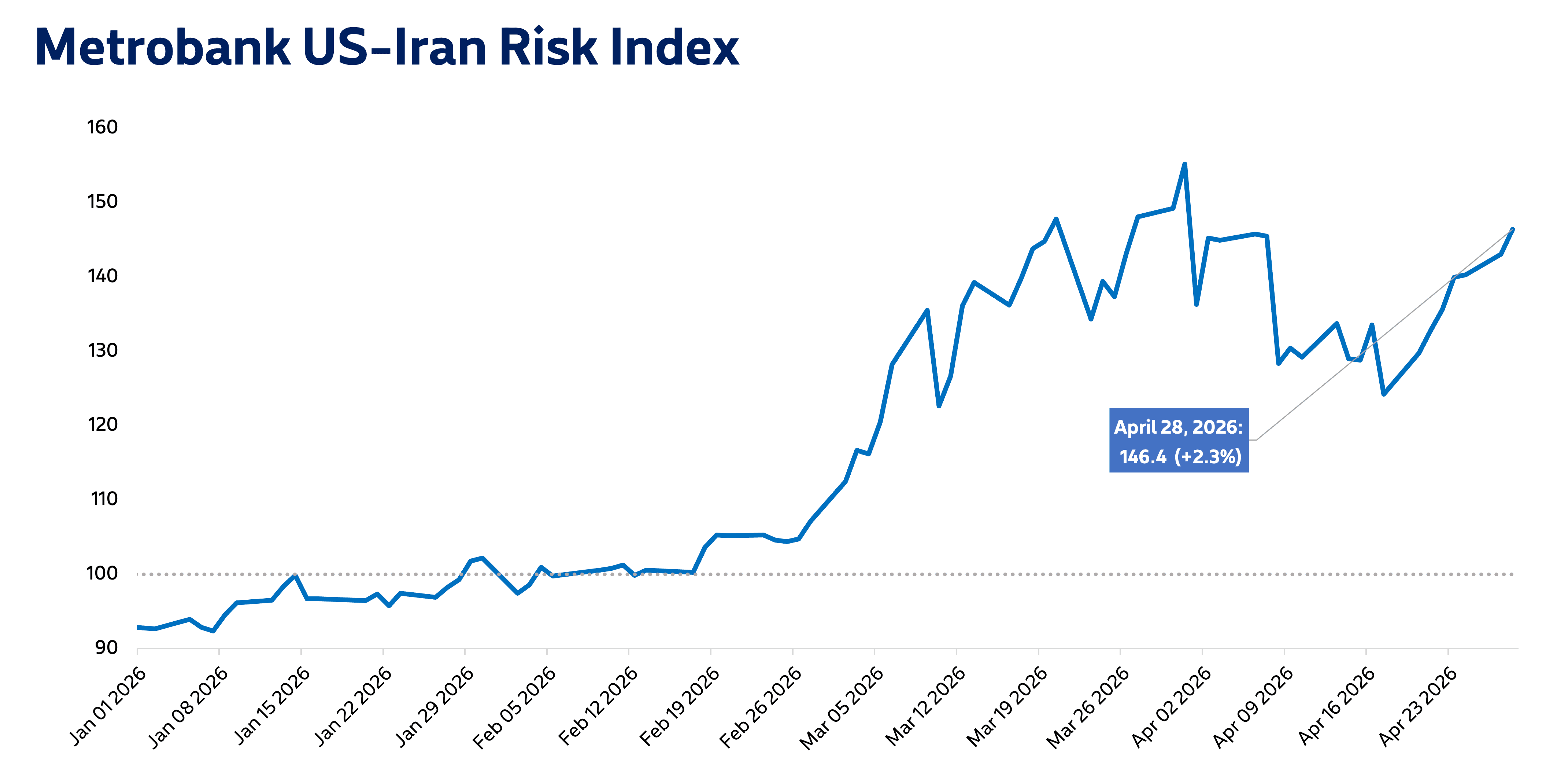

Metrobank US-Iran Risk Index: Oil and currency

The US-Iran war was one of the biggest drivers behind the Philippine Peso’s recent record low.

April 29, 2026 by Metrobank, Investment Counselor Department

Share this article:

Metrobank’s US-Iran Risk Index settled at 146.4 on April 28, 2.3% higher than the prior trading day.

Global oil markets faced downward pressure with news that the United Arab Emirates (UAE) would exit the Organization of the Petroleum Exporting Countries (OPEC), according to Reuters.

While the move led to market players’ expectations of improved oil supply—as the UAE moves away from the OPEC’s production quotas, the Strait of Hormuz’s closure kept the commodity’s price on an upward path. As a result, Brent Crude closed at USD 111 per barrel on Tuesday, according to data compiled by Bloomberg.

Meanwhile, the peso closed at a record low against the US Dollar on Tuesday, Philippine time, with the dollar-peso exchange rate ending the trading day at 61.30. On top of safe-haven demand fortifying the dollar, peso weakness has persisted, as expensive oil pushes import prices higher and foreign investment inflows continue to decline.

Currently, there is still no news on when the US and Iran will resume negotiations. Market players will likely continue to price in higher risk levels for the time being, placing greater pressure on oil and the peso in the coming days.

Metrobank still sees elevated risk and volatility in the near-term, as the path toward a resolution to the conflict remains uncertain. Oil prices are poised to stay high, as global supply remains constricted. Consequently, domestic inflation is expected to quicken on rising local energy prices.

Moreover, the Bangko Sentral ng Pilipinas (BSP) raised its policy interest rate last week to stem rising inflation expectations. Metrobank forecasts at least one more rate hike by the BSP this year. Finally, Metrobank expects the dollar-peso exchange rate to stay elevated, as dollar demand weighs on a weak peso.

Metrobank’s US-Iran Risk Index measures the amount of risk that the ongoing conflict presents to financial markets. It considers the general risk sentiment of investors and inflationary pressure brought by the conflict. A value of 100 denotes a normal level of risk based on market levels prior to the conflict’s escalation, while values greater than 100 imply increasing levels of risk.