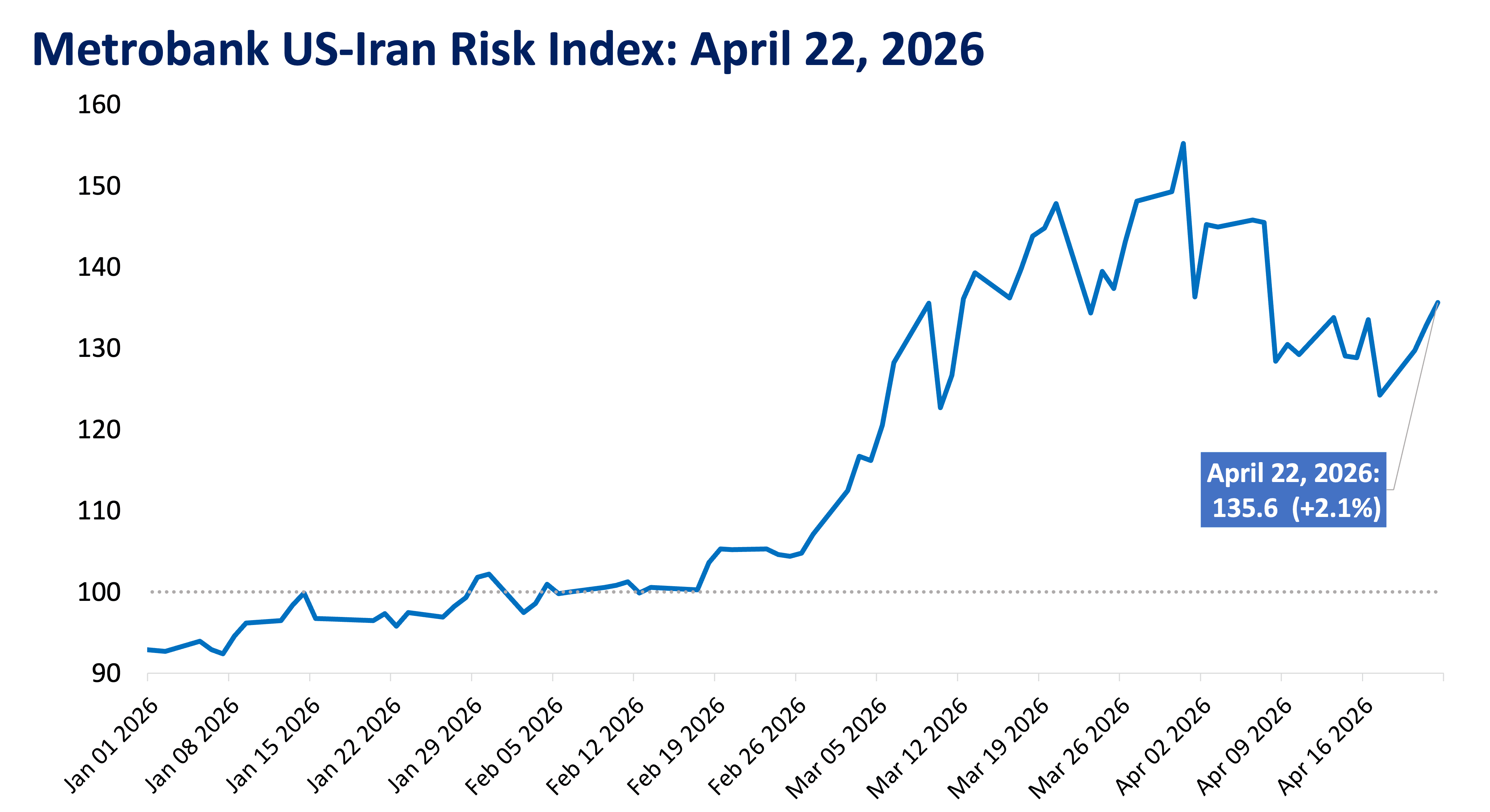

Metrobank’s US-Iran Risk Index settled at 135.6 on April 22, 2026, 2.1% higher than the previous trading day.

The ceasefire’s extension provided little relief to financial market players as oil prices continued to climb. Supply of the commodity has remained tight due to the Strait of Hormuz’s closure and the US’s blockade, exacerbated by reports of Iran’s seizure of two ships passing through the strait, according to Reuters. As a result, Brent crude closed at over USD 100 per barrel for the first time in weeks on Wednesday, according to data compiled by Bloomberg.

These mounting uncertainties led to the US dollar’s continued appreciation due to safe-haven demand, resulting in the dollar-peso exchange rate closing above 60 again on Wednesday. Rising oil prices also led to the benchmark 10-year US Treasury yield moving upward.

A lack of fresh developments in US-Iran talks will likely keep market players more risk-off as they wait for a clearer direction on the war’s possible resolution.

Metrobank still sees high risk and volatility in the near-term, as the path towards a resolution remains uncertain. Oil prices are poised to stay high as global supply remains constricted. Moreover, domestic inflation is expected to accelerate, on rising local energy prices, which will likely compel the Bangko Sentral ng Pilipinas (BSP) to raise its policy interest rate this year. Finally, Metrobank expects the dollar-peso exchange rate to stay elevated, as dollar demand weighs on a weak peso.