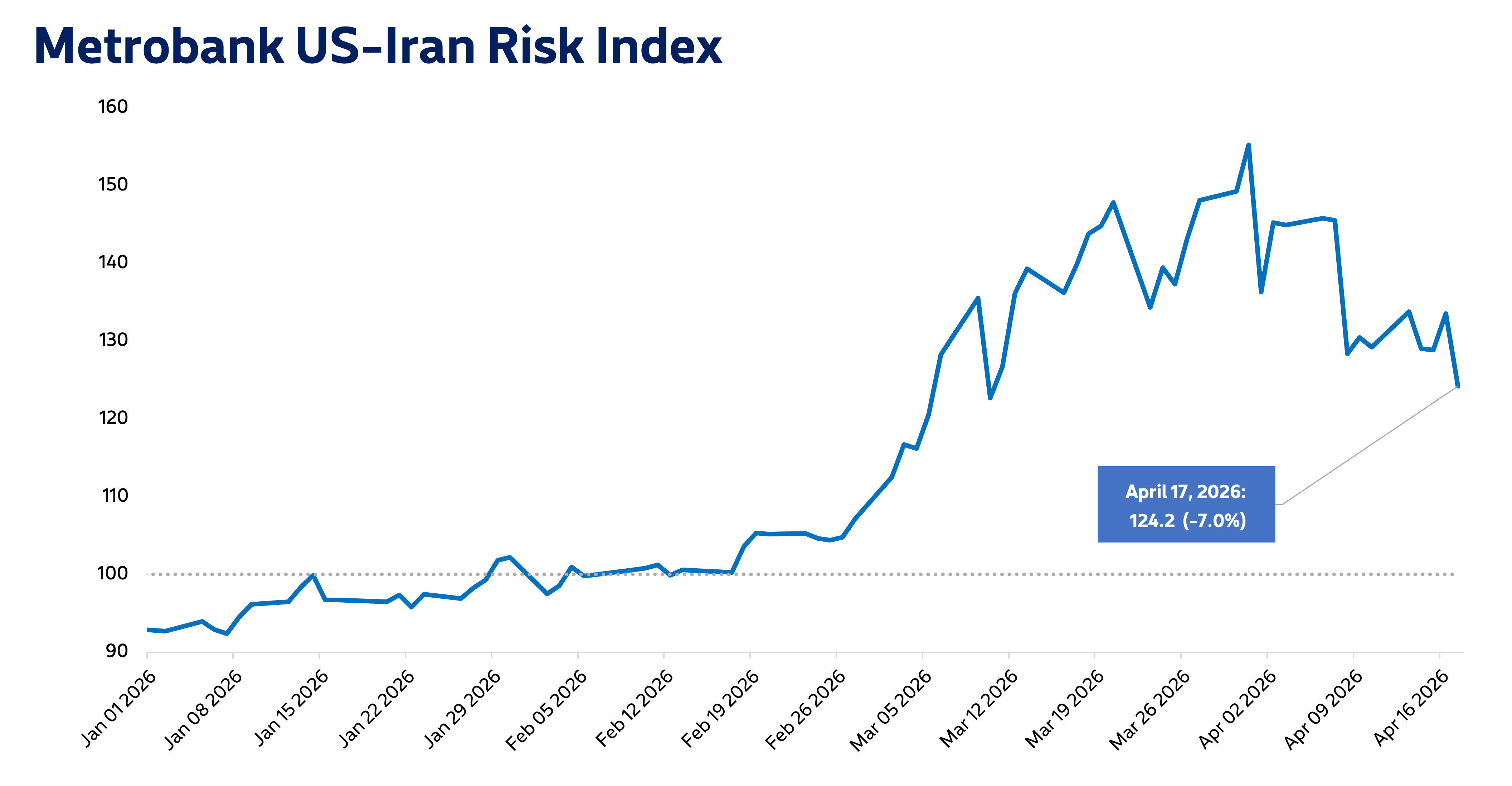

Metrobank’s US-Iran Risk Index settled at 124.2 on April 17, 7.0% lower than the prior trading day and its lowest level in over a month.

Though risk levels eased on Friday due to the Strait of Hormuz’s “reopening,” this was quickly undone over the weekend due to the strait being closed again following the US’s seizure of an Iranian cargo ship. Though Brent crude closed 9.1% lower at USD 90.38 per barrel on Friday, the commodity has already retraced its losses in early Monday trade, opening at USD 96.12, according to data compiled by Bloomberg.

Moreover, the US dollar is also expected to rebound from its downward move last week, as rising risk levels renewed safe-haven flows to the currency. Heightened tensions will also likely elevate the 10-year US Treasury yield going forward, as concerns over faster inflation resurface.

With the Strait of Hormuz closed once again and news that Iran has rejected a second round of talks with the US, according to Reuters, risk levels will likely rise, as tensions reignite. Financial market players are bracing for another turbulent week ahead.

Metrobank still sees high risk and volatility in the near-term. Oil prices are poised to stay elevated, as global supply remains constricted. Moreover, domestic inflation is expected to accelerate, as local energy prices stay high, which will likely compel the Bangko Sentral ng Pilipinas (BSP) to raise their policy interest rate this year. Finally, Metrobank expects the dollar-peso exchange rate to stay elevated, as dollar demand weighs on a weak peso.