Economy3 MIN READ

Metrobank US-Iran Risk Index: Waiting for clarity

Market players have become less optimistic about a lasting deal between the US and Iran.

April 17, 2026 by Metrobank, Investment Counselor Department

Share this article:

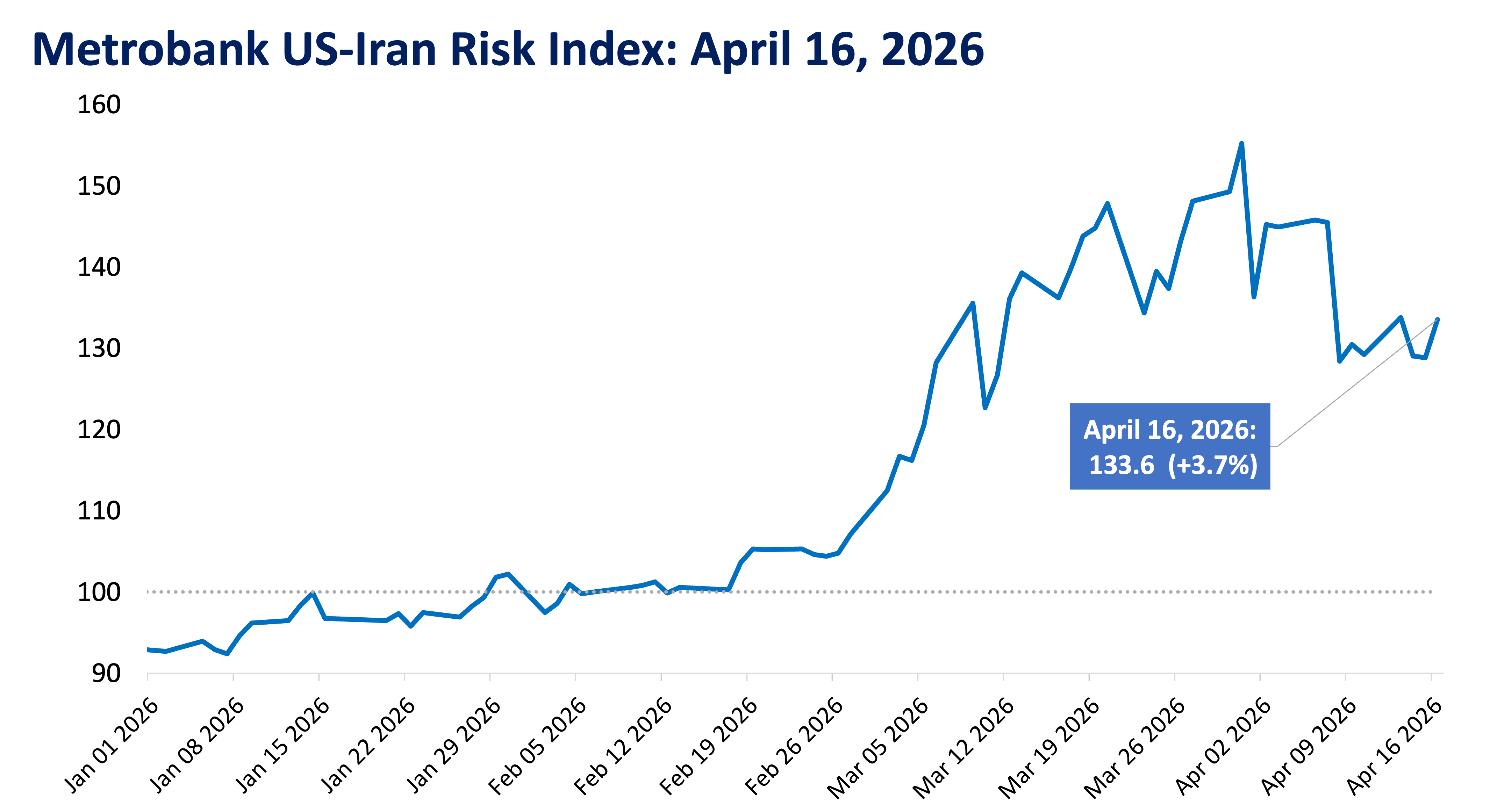

Metrobank’s US-Iran Risk Index settled at 133.6 on April 16, 3.7% higher than the prior trading day.

Risk levels rose as market players became less optimistic about a deal between US-Iran. Brent crude prices rose to just under USD 100 per barrel on Thursday as no developments were reported regarding a resumption of US and Iran talks, despite US President Donald Trump saying he was confident a deal would be reached soon. Markets weighed this against persisting oil supply pressure leading to elevated oil prices.

Meanwhile, the US dollar regained some of its strength as investors moved back into the safe-haven asset while awaiting news of a potential deal. Higher oil prices also pushed the benchmark 10-year US Treasury yield upward by nearly 3 basis points.

Israel and Lebanon agreed to a 10-day ceasefire, which may be a signal towards broader easing of tensions in the Middle East. Still, concrete developments between the US and Iran will likely remain the largest driver of risk sentiment among market players in the coming days.

Metrobank still sees high risk and volatility in the near-term. Oil prices are poised to stay high as global supply remains constricted. Moreover, domestic inflation is expected to accelerate, as local energy prices stay high, which will likely compel the Bangko Sentral ng Pilipinas (BSP) to raise their policy interest rate this year. Finally, Metrobank expects the dollar-peso exchange rate to stay elevated, as dollar demand weighs on a weak peso.

Metrobank’s US-Iran Risk Index measures the amount of risk that the ongoing conflict presents to financial markets. It considers the general risk sentiment of investors and inflationary pressure brought by the conflict. A value of 100 denotes a normal level of risk based on market levels prior to the conflict’s escalation, while values greater than 100 imply increasing levels of risk.