Economy3 MIN READ

Metrobank US-Iran Risk Index: Starting over

Market players look toward a potential resumption of talks between the US and Iran.

April 16, 2026 by Metrobank, Investment Counselor Department

Share this article:

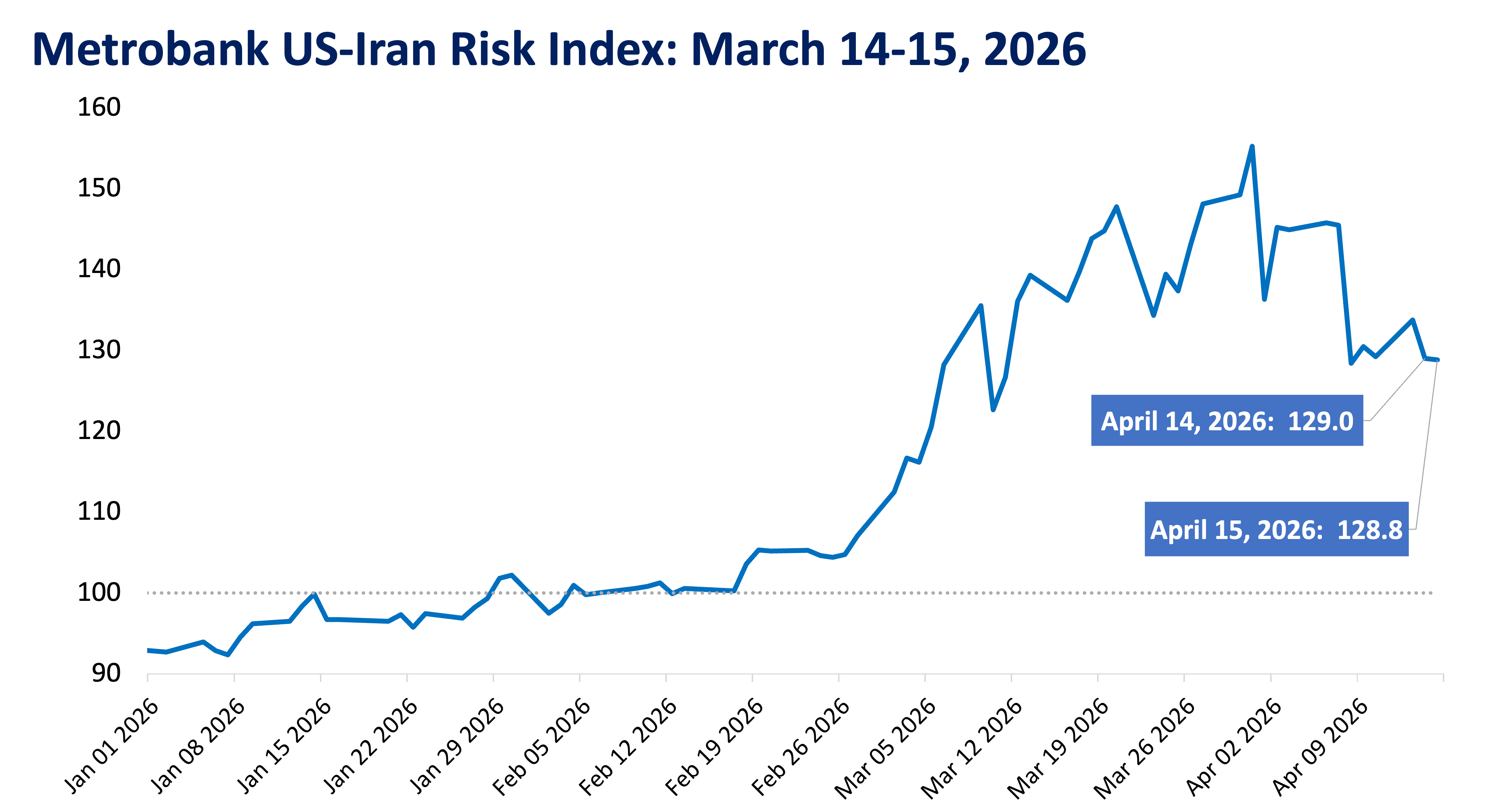

Metrobank’s US-Iran Risk Index settled at 128.8 on April 15, 0.2% lower than its value of 129.0 on April 14.

Oil prices moved downwards on Tuesday and held steady on Wednesday as market players remained optimistic about a potential deal between the US and Iran. This comes after a report from Al Jazeera that a Pakistani delegation was in talks with Iran to pursue another round of negotiations with the US. Brent crude, the benchmark for global oil prices, closed at nearly USD 95 per barrel as a result.

Moreover, the dollar index reached its lowest value in over a month, according to data compiled by Bloomberg, as market optimism for a deal led to reduced demand for the currency as a safe haven. Meanwhile, the benchmark 10-year US Treasury yield rose marginally by nearly 4 basis points as investors held their breath for news of a deal on the horizon.

Market players will keep monitoring news on the state and direction of US-Iran negotiations, which will continue to drive the general risk appetite and sentiment of investors in the days ahead.

Metrobank still sees high risk and volatility in the near-term as market players’ moves will likely be in reaction to headlines and developments in the conflict. Oil prices are poised to stay high as global supply remains constricted. Moreover, domestic inflation is expected to accelerate, as local energy prices stay high, which will likely compel the Bangko Sentral ng Pilipinas to raise its policy interest rate this year. Finally, Metrobank expects the dollar-peso exchange rate to stay elevated, as dollar demand weighs on a weak peso.

Metrobank’s US-Iran Risk Index measures the amount of risk that the ongoing conflict presents to financial markets. It considers the general risk sentiment of investors and inflationary pressure brought by the conflict. A value of 100 denotes a normal level of risk based on market levels prior to the conflict’s escalation, while values greater than 100 imply increasing levels of risk.