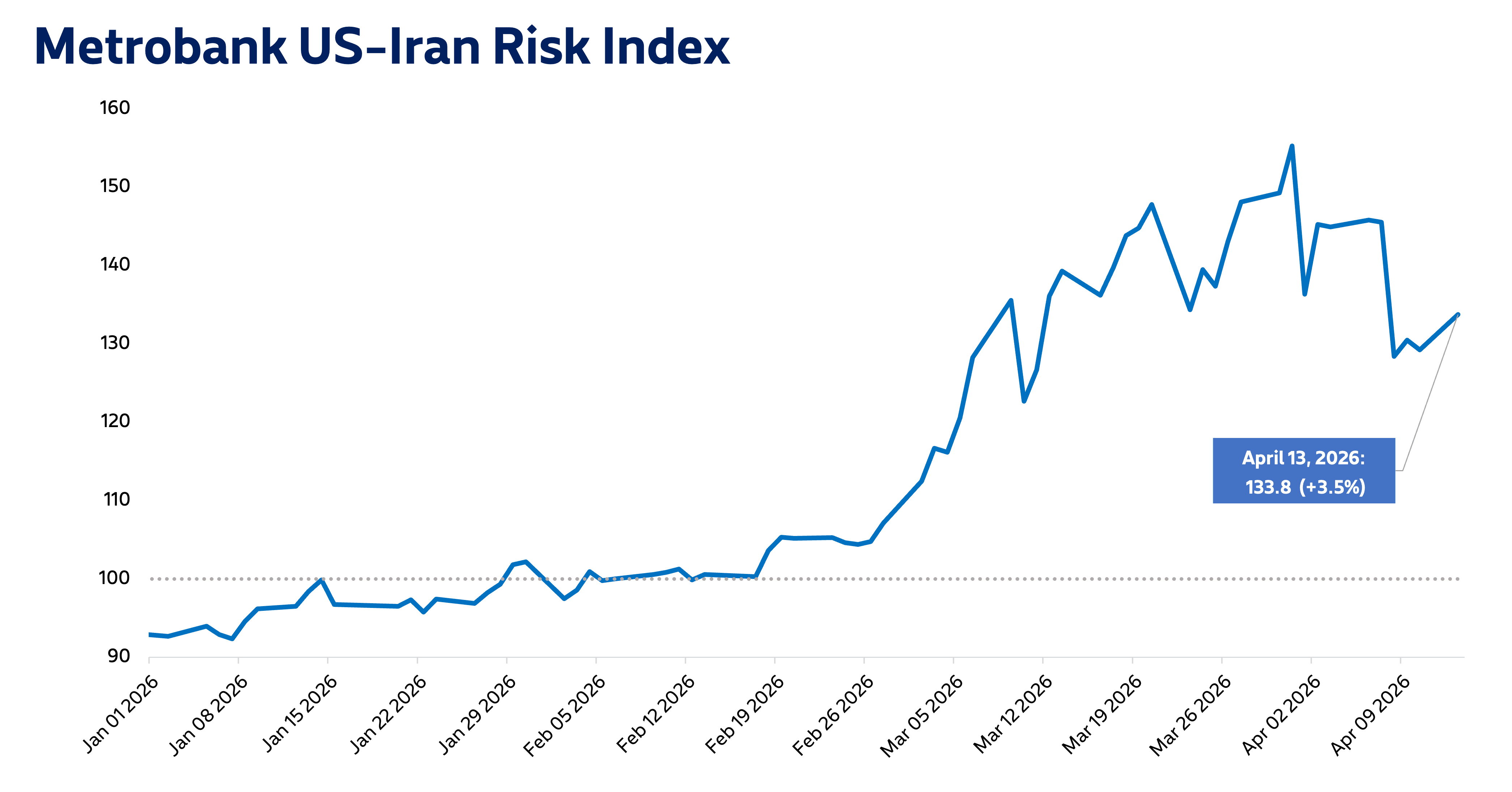

Metrobank’s US-Iran Risk Index settled at 133.8 on April 13, 3.6% higher than its value of 129.2 on April 10.

Risk levels rose after the US and Iran failed to reach an agreement over the weekend due to Iran refusing to accept Washington’s terms for the deal, according to Al Jazeera. Soon afterward, US President Donald Trump announced a blockade of the Strait of Hormuz, a critical passageway for global shipments that the US has been working to reopen. The US Central Command clarified that this blockade would only affect ships entering and exiting Iranian ports, according to NBC News.

Financial market players priced in the lack of a deal and continued oil supply constraints, with Brent crude moving above USD 100 per barrel during early Monday trade. The commodity eventually closed below USD 100 following statements from Trump that Iran still wants to work out a deal, according to Al Jazeera.

The US dollar’s strength also slightly waned, as investors’ hopes for a deal to be struck soon led to reduced safe-haven flows to the currency. Moreover, the benchmark 10-year US Treasury yield edged lower as inflation expectations moderated.

Metrobank still sees high risk and volatility in financial markets as the conflict develops. Oil prices will still likely stay high as supply remains constricted. Moreover, domestic inflation is expected to accelerate, as local energy prices stay high, which will likely compel the Bangko Sentral ng Pilipinas (BSP) to raise their policy interest rate this year. Finally, Metrobank expects the dollar-peso exchange rate to stay elevated, as dollar demand weighs on a weak peso.