Economy3 min read

Metrobank US-Iran Risk Index: Mounting tensions

As the Middle East conflict rages on, risk levels remain high.

March 18, 2026 by Metrobank, Investment Counselor Department

Share this article:

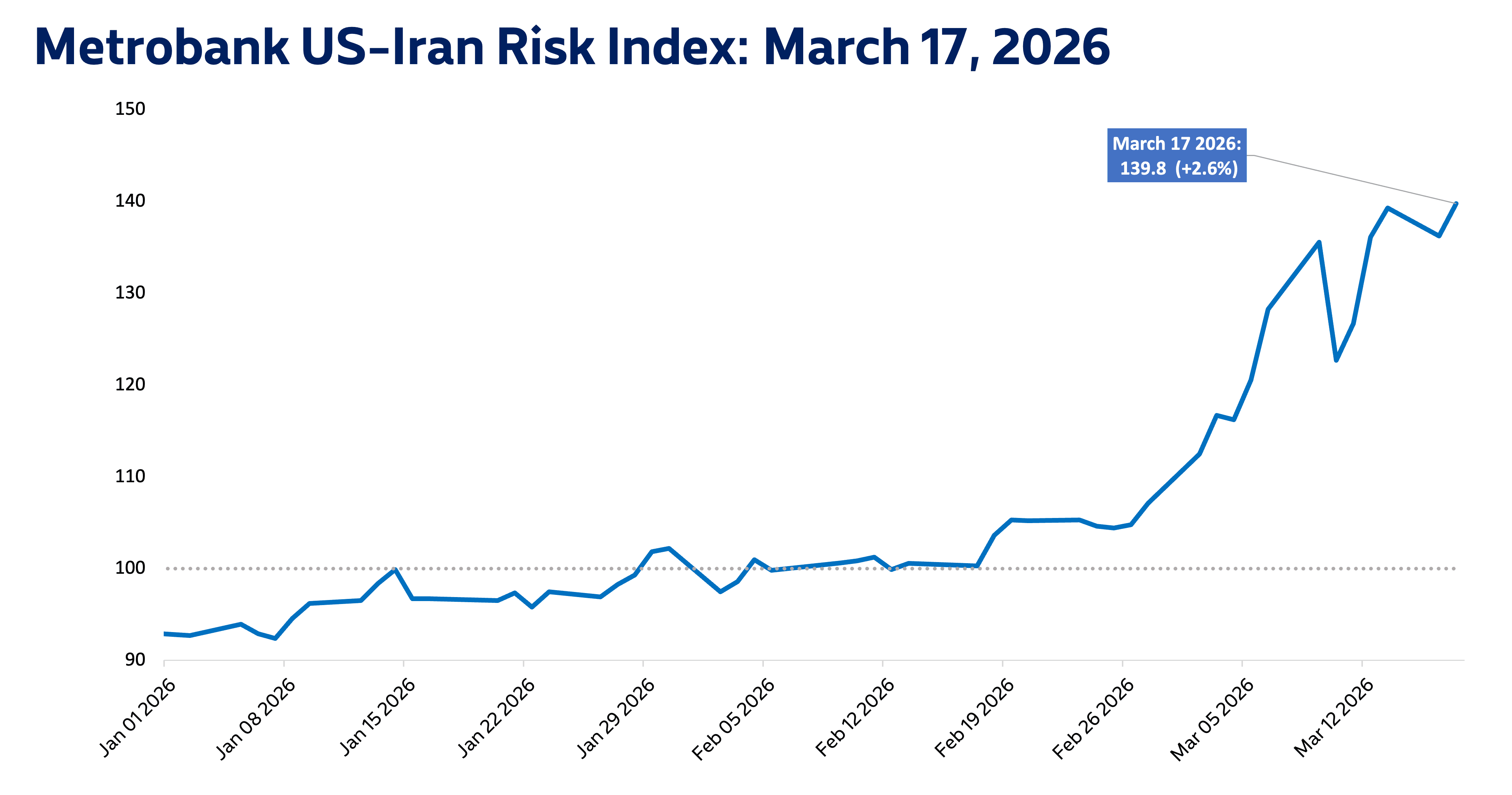

Metrobank’s US-Iran Risk Index settled at 139.8 on March 17, 2026, 2.6% higher than the previous day.

Oil prices rose on Tuesday, as the conflict in the Middle East continued. Projectiles hit United Arab Emirates’ Fujairah port, a key oil facility for the country, and surrounding areas, according to media reports.

Brent crude settled higher at USD 103.42 per barrel, one of its highest levels since the conflict first erupted, according to data compiled by Bloomberg.

Meanwhile, dollar strength continued to soften on Tuesday, with the US dollar index settling lower. While markets are still very volatile, this may be a sign of investors leaning slightly more risk-on, leading to reduced safe-haven demand for the currency. The benchmark 10-year US Treasury yield also settled lower, possibly indicating investors pricing in less inflation risk.

Still, for as long as the Strait of Hormuz stays closed, market risk remains high. Moreover, Iran has vowed to retaliate after the death of its security chief, according to the BBC. This risks further escalation of the conflict.

Metrobank maintains its expectation for upside oil risk to endure, as the Middle East conflict rages on. Domestically, while a potential removal of fuel excise taxes will provide some relief to Filipino consumers, local inflation is still expected to accelerate as oil prices rise. We expect this to prompt the Bangko Sentral ng Pilipinas (BSP) to preemptively end their easing cycle this year. Additionally, dollar strength will persist, as safe-haven demand continues. This puts pressure on the peso and will keep the dollar-peso exchange rate elevated in the near future.

Metrobank’s US-Iran Risk Index measures the amount of risk that the ongoing conflict presents to financial markets. It considers the general risk sentiment of investors and inflationary pressures brought on by the conflict. A value of 100 denotes a normal level of risk based on market levels prior to the conflict’s escalation, while values greater than 100 imply increasing levels of risk.