DOWNLOAD

DOWNLOAD

Metrobank US-Iran Risk Index: No time to settle down

Financial markets stayed on edge as chances for an immediate end to the conflict became slim.

By Metrobank Research, Investment Counselor Department

By Metrobank Research, Investment Counselor Department

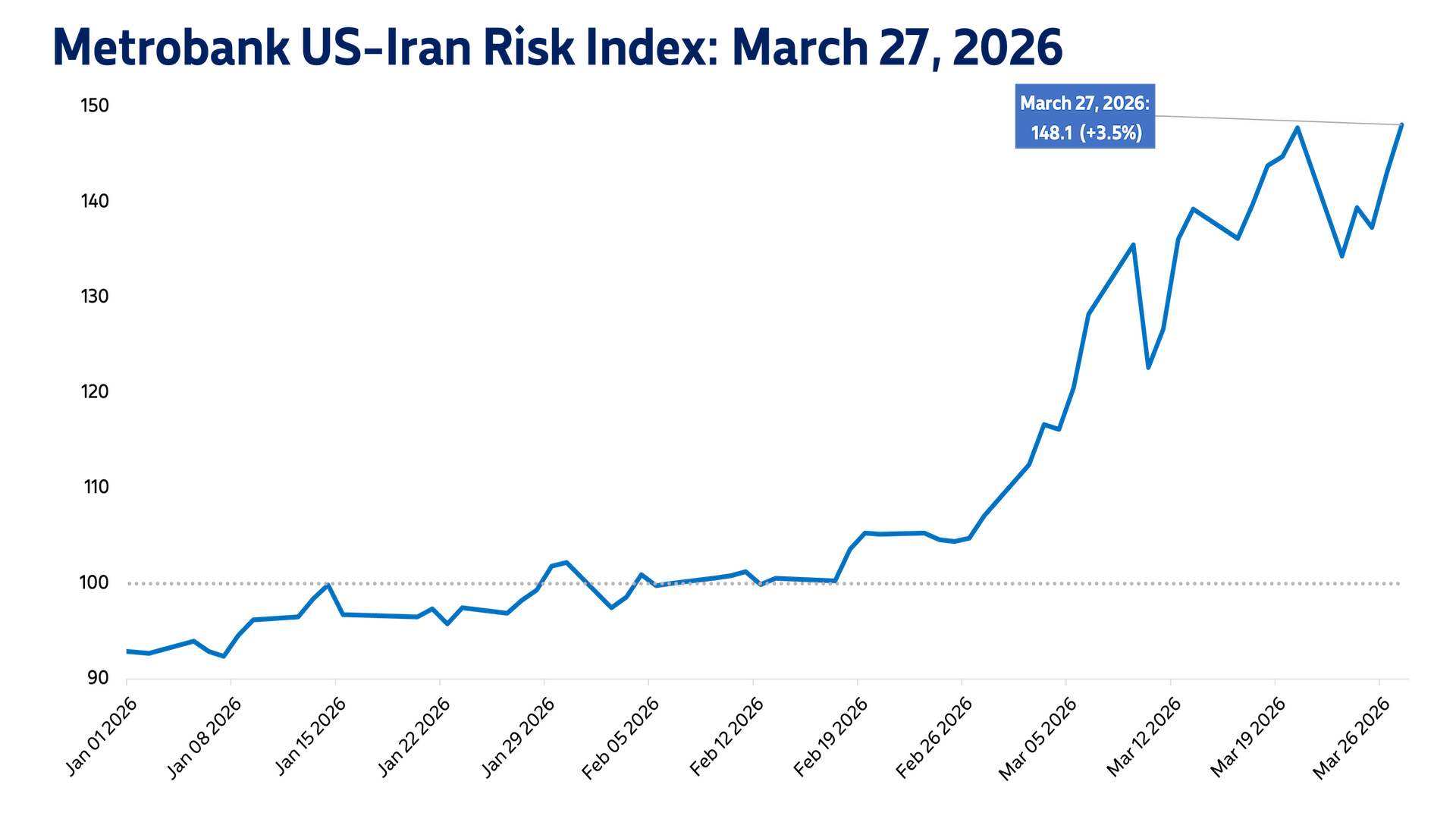

Metrobank’s US-Iran Risk Index settled at 148.1 on March 27, 2026, 3.5% higher than the previous day. This marks a new all-time high for the index.

Financial market players were little swayed by US President Donald Trump’s announcement of an extension on its pause on Iran strikes until April 6, as they priced in higher risk from the Strait of Hormuz remaining closed and continued military attacks in the Middle East. Brent crude settled at USD 112.57 per barrel on Friday, its highest price since the conflict erupted, according to data compiled by Bloomberg.

Higher oil prices continued to add upward pressure to yields, with the benchmark 10-year US Treasury yield moving higher. The US dollar has also continued to strengthen on safe-haven flows, putting pressure on the peso. The dollar-peso exchange rate consequently ended the Philippine trading day at 60.55, a historical low for the peso’s close.

Friday’s market movements may indicate that financial market players have become less confident in the war’s immediate resolution. Unless any concrete developments for the war’s end take place—and confirmed by both sides of the conflict, upside oil risk will likely endure and add pressure to global inflation.

Metrobank still sees continued upside oil risk, as the Strait of Hormuz, a critical transit point for global oil shipments, remains closed. We also expect the Bangko Sentral ng Pilipinas to raise their policy rate this year to combat rising inflation. Lastly, we see the dollar-peso remaining elevated in the near-future, as the dollar continues to strengthen on safe-haven demand.

Metrobank’s US-Iran Risk Index measures the amount of risk that the ongoing conflict presents to financial markets. It considers the general risk sentiment of investors and inflationary pressure brought by the conflict. A value of 100 denotes a normal level of risk based on market levels prior to the conflict’s escalation, while values greater than 100 imply increasing levels of risk.

What now?

| Asset Class | Outlook | Strategy |

|---|---|---|

| Local Fixed Income | Bearish | Stay defensive on duration amid elevated foreign exchange volatility. Focus on liquid 2–5-year tenors and add only on pronounced yield spikes. Avoid extending duration, especially at the long end of the yield curve, until peso conditions and global risks show clear signs of stabilization. |

| Local Equities | Bearish | Expect bargain hunting of cheaper names in the near term. However, gains may remain capped amid oil-price volatility and developments in the Middle East. Buy on dips and take profit during rallies. |

| Global Fixed Income | Bearish | Continue to favor short-dated quality bonds up to 5 years, as inflation fears push yields upward. Expect yields to stay elevated, as geopolitical tensions keep investors cautious. |

| Global Equities | Neutral | Maintain a defensive approach by prioritizing high-dividend sectors while taking advantage of volatility to accumulate select quality-growth names. |

| USD/PHP | Rangebound | Buy US dollars on dips or near the 59.85-60.15 support levels, as short-term fundamentals favor a mildly firmer USD after the US Federal Reserve (Fed) maintained its policy. Still, elevated energy prices and geopolitical risk will provide demand for USD. The market is expected to trade on headlines for the lack of high-impact US and Philippine data release this week. |

| G10 Currencies / US Dollar | Bearish | Major currencies EUR, GBP, and JPY see some recovery following their respective central banks’ decision to pause. However, inflation concerns driven by higher-for-longer oil prices continue to weigh on global growth prospects, weakening G10 economies dependent on energy imports while safe-haven trades favor the USD. |

| Gold | Bearish | Consistently elevated oil prices have driven hotter US inflation and delayed Fed rate cut expectations, contributing to a stronger US dollar and lower gold prices. The precious metal has broken through key levels below USD 5,000 but saw strong support from bargain hunters at the USD 4,100 level. Gold has since recovered back to between USD 4,400 to 4,600, which are good levels to pick up, but we prefer opportunities to pick up closer to USD 4,000, should hostilities escalate further. Our long-term view is still for gold to outperform as global central banks diversify their reserve assets away from USD and US Treasuries. |

(Disclaimer: This is general investment information only and does not constitute an offer or guarantee, with all investment decisions made at your own risk. The bank takes no responsibility for any potential losses.)